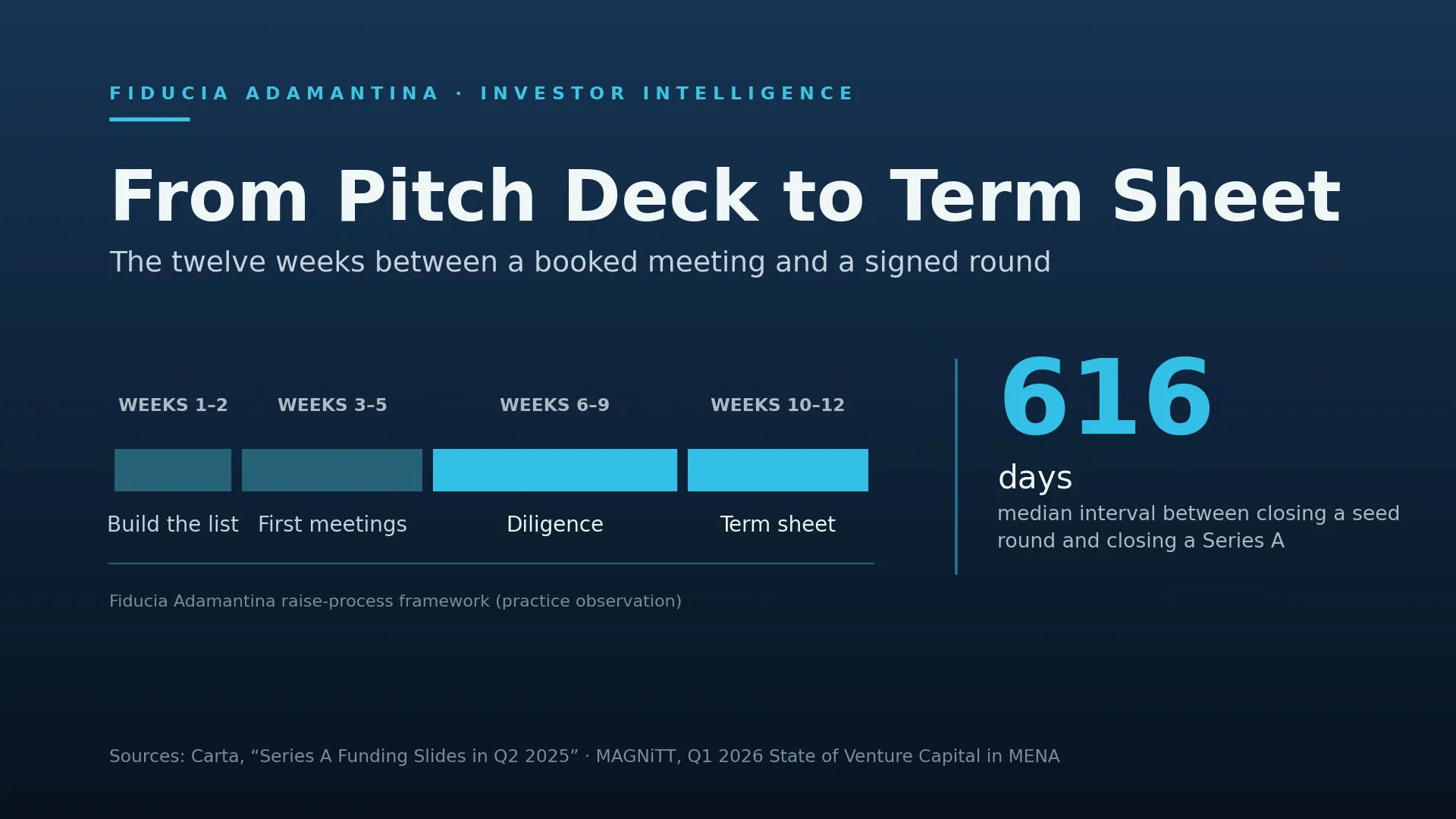

Carta’s data puts the median gap between closing a seed round and closing a Series A at 616 days — a little over twenty months, and more than two months longer than it was two years earlier (Carta, Q2 2025). That number is not a measure of how long a raise takes. It is a measure of how long founders now spend getting ready for one.

The raise itself is shorter and stranger than most founders expect, and far more procedural. Founders come to me with meetings already in the diary and no idea what the next twelve weeks contain: how long an investor takes to say no, what silence means, what happens between the pitch and the paperwork, and what a term sheet actually settles.

Here is the map. Twelve weeks, phase by phase, with the failure modes named.

The round starts long before the first meeting

Nearly all of the work that decides your round is done before an investor has seen a slide.

Two facts set the frame. First, runway. Begin a raise with fewer than six months of cash and you are not negotiating, you are asking to be rescued, and every investor on your list can read the difference in your urgency. Nine to twelve months of runway at kickoff is the working floor in our practice: enough to survive a failed first process and start a second.

Second, the market you are actually raising into. MAGNiTT’s Q1 2026 read on MENA venture found deal activity at its weakest quarterly level in five years even as total funding rose double-digits quarter-on-quarter, concentrated into fewer and larger rounds at record average cheque sizes, with international investors stepping back (MAGNiTT, Q1 2026). Saudi Arabia in the same quarter saw deal volume fall 39% year-on-year and funding fall 62% (MAGNiTT, Q1 2026 KSA).

Fewer deals are getting done, and the ones that do are bigger and more heavily scrutinised. A concentrated market does not reward a broad, hopeful process. It rewards a narrow, evidenced one.

If you are still deciding whether you are ready to start, the honest answer usually surfaces in the five-minute investor-readiness self-assessment. If you want the mechanics of raising in this region first, our step-by-step guide to raising funding in the UAE covers the ground beneath this article.

Weeks 1–2: the list is the strategy

Most founders treat the investor list as an output of the raise. It is the raise.

In this phase you are doing three things. You are building a target list of 30 to 50 named funds and family offices where the fit is real: stage, cheque size, sector, geography, and whether they have deployed in the last two quarters. You are mapping the warm path to each one, because the cold-inbound conversion rate for a first-time founder is close enough to zero that it should not be the plan. And you are sequencing — the investors you most want should not be the first ones you meet.

That last point costs founders more than any other. Your pitch improves through repetition. Burn your top five names in week one and you have spent your best relationships on your worst version of the story.

Practice observation: the founders who close fastest build the list from relationship reality, not fund reputation. A warm introduction to a mid-tier fund converts better than a cold approach to a famous one, every single time.

Weeks 3–5: first meetings, and what happens between them

You will feel like you are being evaluated in the room. You are not, or not mainly.

What actually happens after a good first meeting is that a partner or principal takes your story into an internal conversation you never see. They pressure-test the market size against their own thesis. They ask a portfolio founder in an adjacent space whether your numbers are plausible. They check whether anyone else on the list has already passed on you, because passes travel between funds faster than intros do.

This is why silence is not neutral. In our practice, a fund that is genuinely interested moves inside ten working days: a second meeting, an analyst asking for the model, a request for customer references. Two weeks of quiet after a “great meeting” is a soft no that has not been typed yet. Do not spend your week interpreting it. Do send one clean follow-up with a specific update, and then move on.

Expect a rough conversion: of 40 well-targeted approaches, perhaps 15 take a first meeting, perhaps 6 take a second, perhaps 2 reach a partner or investment-committee conversation. If you want one term sheet, you need to run the top of that funnel wide enough to survive it. And the deck has to survive it too. Most do not — the pitch deck mistakes that turn off GCC investors are almost all failures of evidence, not design.

Because every one of these meetings is expensive and unrepeatable, walk into each one the same way. Our free Pre-Meeting Investor Checklist is the thirteen-point list we run in the twenty-four hours before an investor call: the night-before, two-hours-before, and fifteen-minutes-before checks. It is the cheapest insurance available against losing a meeting you had already earned.

Weeks 6–9: diligence is a stress test of your own claims

Diligence does not discover new things about your company. It tests whether the things you already said are true.

The pattern is consistent. An investor takes the three or four load-bearing claims from your pitch — the growth rate, the retention, the pipeline, the unit economics — and tries to reproduce them from primary evidence. Bank statements against revenue. Cohort exports against the retention chart. Signed contracts against the pipeline slide. Named customers who will take a call.

Where founders lose the round here is almost never fraud. It is drift: the deck says 4% monthly churn, the raw export says 6.5%, and nobody had reconciled the two because the deck number came from a board pack that used a different definition. The investor does not conclude that you have higher churn. They conclude that your numbers cannot be trusted, which is a much more expensive conclusion.

Two rules. Every number in the deck must be reproducible from a source file you can send within an hour. And the model an investor receives must be the model you actually run the business against, with the assumptions visible and defensible, not a growth curve reverse-engineered from the raise size.

Weeks 10–12: the term sheet settles less than you think

A signed term sheet is the beginning of the legal process, not the end of the raise. It is mostly non-binding. It converts into money only after definitive documents, confirmatory diligence, and, on a priced round, a set of agreements that take weeks to negotiate.

What matters is that the term sheet fixes the terms you will live inside for years, and it does so at the exact moment your leverage is highest and your attention is lowest. Founders sign in relief. That is the mistake.

Read the economics before the headline. Valuation is the number founders discuss and the one that determines the least. The liquidation preference, the option pool and whether it is created pre- or post-money, the anti-dilution mechanic, the board composition, the consent rights over what you can do without an investor’s permission: these decide what the round costs you. We set out what the arithmetic does to founder ownership in the GCC founder dilution benchmark.

Get a specialist lawyer on the document before you sign anything, including the exclusivity clause. Exclusivity ends your process: once you sign, you cannot talk to anyone else, and if the deal collapses in confirmatory diligence you restart a raise with less runway and a story about a failed round.

The calendar gaps that catch Gulf-corridor rounds

If you are raising into GCC capital, the calendar is a live risk that global fundraising advice will not tell you about.

Gulf summer is real. From late June through August, decision-makers travel and committee cadence thins. A process that is mid-diligence in July does not die, but it stretches: in our practice, by three to five weeks nobody planned for.

Ramadan compresses working hours and moves earlier each year. In 2027 it is expected to begin in early February, subject to moon sighting. A raise launched in December aiming to close in the first quarter runs directly into it.

And family-office capital, a large part of what founders actually raise in this region, does not run on a fund’s clock. There is no committee calendar to plan against. Decisions arrive in a week or sit for a quarter, and the deciding conversation frequently happens in a room you are not in. Build the relationship earlier than you think you need to, and never make a family office the only path to your close.

Where rounds actually die

Four failure modes, in the order I see them.

The founder starts too late. Six months of runway becomes four during the process. The raise is now visible to investors as distress, and the terms reflect it.

The story is not consistent across the materials. The deck says one thing, the model implies another, the data room says a third. Nobody is lying; nobody reconciled.

The process is sequential instead of parallel. A round closes because several investors converge on the same window. Run investors one at a time and you do not have a round, you have a series of conversations.

The founder negotiates the valuation and ignores the structure. A headline number wins the announcement and loses the exit.

None of these is a market problem. All four are preparation problems, solvable before a single meeting is taken.

What to have built before you start

If you have meetings already in the diary, the immediate step is the free Pre-Meeting Investor Checklist above. Run it before the next call.

Underneath the checklist sits the harder question: are the materials themselves good enough to carry twelve weeks of scrutiny? A pitch deck that survives a first meeting is not the same asset as a model that survives diligence, and most founders discover the gap at week seven, when it is expensive.

That is the problem the Investor Readiness Sprint exists to solve. It is a fixed-fee build, not a consulting relationship: AED 25,000, 50% at kickoff and 50% on delivery, 2–3 weeks from complete intake. You get the deck, a management-input operating model with sensitivities and use of funds, one post-raise cap-table scenario, the founder narrative and objection notes, a live rehearsal, and an editable handover pack. It is bought on its own terms. No mandate, no success fee, no obligation afterwards.

What it is not: the Investor Readiness Sprint builds the materials that carry your raise. It does not build your data room, cure legal or accounting gaps inside the company, introduce you to investors, or guarantee a term sheet. What it does is make sure that when the meetings you have already booked turn into diligence, the evidence holds.

If you have a raise starting in the next quarter and you are not certain the materials will survive it, book an IRS Strategy Call. Thirty minutes, free, and you will leave it knowing whether the build is worth doing. Engagement details are on the Investor Readiness Sprint page.

Twelve weeks is enough time to close a round. It is not enough time to become worth investing in. That work happens first, or it does not happen at all.