You own 62% of your company on paper. You are raising a round that, on the term sheet, sells 20% to a new investor. So you will own about half afterwards, give or take. That is the arithmetic most founders run in their head, and in a real deal it is wrong by more than ten percentage points.

The founder I have in mind said it almost exactly this way: “I own 62%. After this round, the option-pool top-up, and two SAFEs converting, apparently I’ll own 37%. Nobody walked me through that math.” He was not bad at numbers. He had modelled the 20% round correctly. What nobody had shown him was that three separate things dilute a founder at a priced round, they land at the same closing, and the term sheet only labels one of them.

This post walks the other two out into the open, with a worked example and what the benchmarks actually say about how much founders keep. Take one thing from it: the number on the term sheet is not the number you end up owning, and the gap is knowable in advance.

The number you were quoted is not the number you keep

A priced round quotes you a headline: money in, pre-money valuation, the investor’s stake. “$3 million at $12 million pre.” The investor buys 20% of the company at close. Clean.

Three things sit underneath that headline and none of them are in the number the investor said out loud. The new option pool the investor requires. The SAFEs you raised eighteen months ago, now converting into shares. And the fact that all of this compounds off your slice specifically, because you are the shareholder with the most to give. Each is standard. Each is negotiable. Together they are the difference between the 50% you expected and the 37% you get.

Surprise one: the pre-money option pool comes out of your slice, not theirs

Almost every priced round requires an option pool for future hires, and the investor almost always wants it expanded to somewhere between 10% and 20% of the company before they wire the money. The phrase to watch on the term sheet is “on a fully diluted, post-money basis” attached to the pool.

Here is what that phrase does. A pool created out of the pre-money valuation is carved from the existing shareholders, which is mostly you. A pool created out of the post-money would be shared with the incoming investor. Investors ask for the pre-money version by default, because it protects their stake and quietly enlarges the pre-money share count they are buying into. On a $12 million pre-money round, moving a 15% pool from pre-money to post-money is worth a meaningful slice of your company, and it is one of the few genuinely negotiable lines on the sheet.

Most founders read the pool as a cost of hiring. It is also a cost of the round, paid entirely by the people already on the cap table.

Surprise two: SAFEs don’t dilute each other, they dilute you

The Simple Agreement for Future Equity was designed to make early raising fast. It succeeds, and it hides its cost until conversion. When you sign a SAFE, no shares change hands and your ownership percentage does not move. The dilution is real but deferred to the day the SAFE turns into stock, which is usually your next priced round.

Two features make the bill larger than founders expect. First, valuation caps. A SAFE with a $6 million cap that converts at a $12 million round buys shares as if the company were worth $6 million, so that investor gets roughly twice the equity the headline round price implies. Second, and this is the one that catches people, the post-money SAFE. Under the common post-money structure, each SAFE holder’s percentage is locked in and protected from the other SAFEs. Raise four small SAFEs at four different caps and none of them dilutes another. The only shareholder absorbing all of them is you.

So the two “small” cheques from eighteen months ago are not small at conversion. They are a pre-committed slice of your Series A cap table that you agreed to before you knew the round price, and they come out of the founders’ column.

Surprise three: the round math is cumulative, and it compounds

Founders model dilution one event at a time and then stop. The real cap table applies them in sequence, and each event shrinks the base the next one works from.

The SAFEs convert: more shares, your percentage lower. The pool is topped up out of the pre-money: more shares again, lower again. Then the new money comes in and dilutes everyone, including the SAFE holders and the pool, but starting from a base where your slice is already smaller than you pictured. Twenty per cent of a company you own less of is a bigger bite of what is left of you.

This is why “62% minus a 20% round is about 50%” fails. That subtraction assumes the round is the only event and that it hits everyone equally. Neither is true.

A worked example: 62% on paper, 37% at close

Here is the stack, worked end to end. The numbers are illustrative, chosen to be clean, but the arithmetic is exact and the sequence is how a real close runs.

Start with a fully diluted cap table before the round: founders 62%, seed angels 28%, an existing 10% option pool. There are two SAFEs outstanding, $750,000 at a $6 million cap and $500,000 at a $9 million cap. The Series A is $3 million at $12 million pre-money, so the investor takes 20% at close, and the investor requires the option pool topped up to 15% of the post-money company, created pre-money.

Watch the founder’s number move:

- Start: 62%.

- The two SAFEs convert. They buy in at their caps, adding shares ahead of the new money. Founder ownership falls to about 52% before the investor has wired a dirham.

- The pool is topped up to 15%, out of the pre-money. More shares, all absorbed by existing holders. Founder ownership falls to about 47%.

- The new money comes in at 20%. Founder ownership settles at about 37%.

The founder expected 62% minus a 20% round, which is roughly 50%. The real answer is 37%. That is a thirteen-point gap, and every point of it was visible in the term sheet and the old SAFE documents before anyone signed. This is the same quiet arithmetic that turns a clean-looking cap table into a diligence problem later, which I wrote about in cap table red flags in MENA fundraising. The structures that scare investors are usually the ones the founder never modelled.

What the benchmarks actually say, and what the Gulf doesn’t have

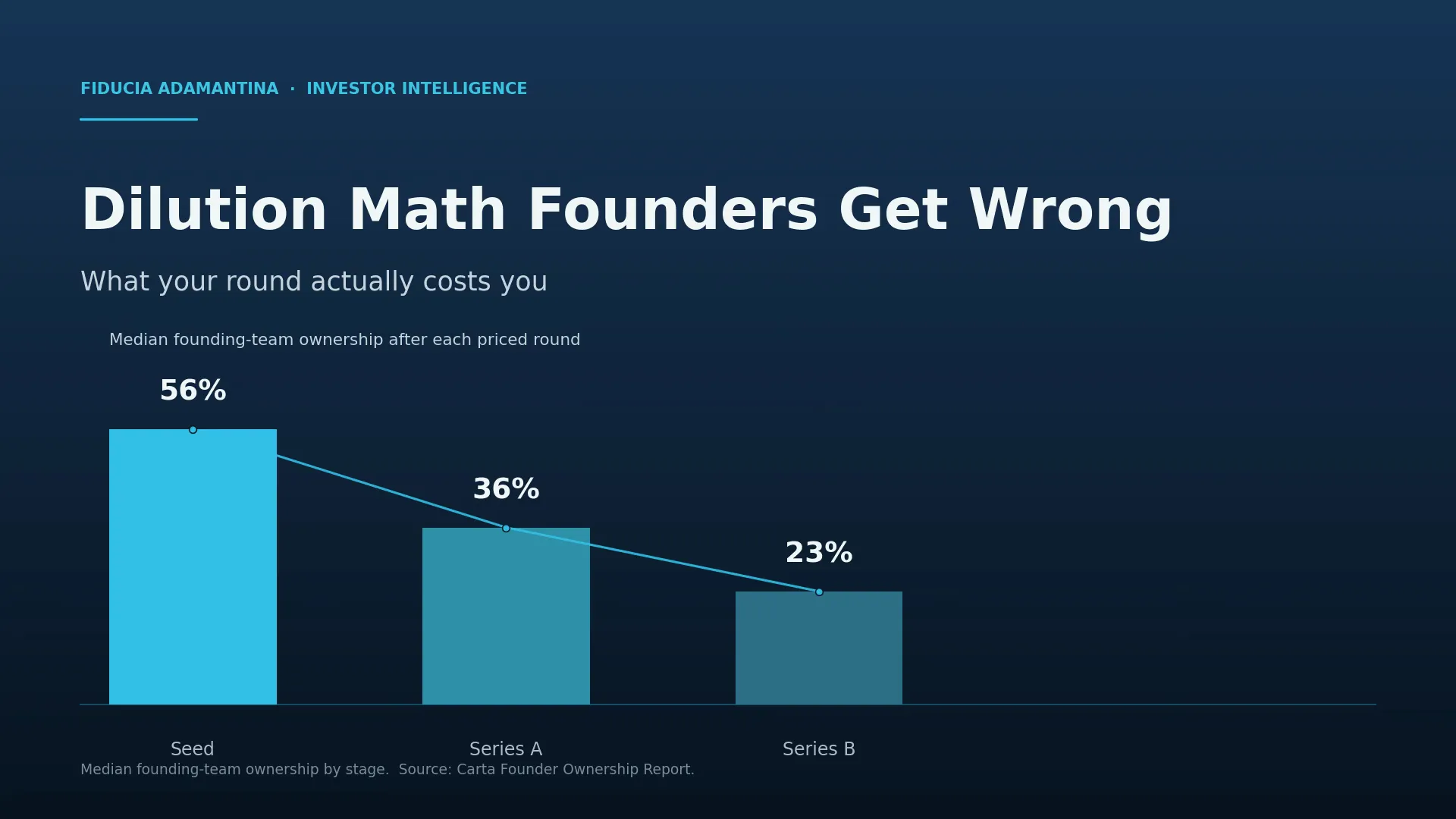

The 37% is illustrative, but the shape is not unusual. On the best primary data available, the Carta Founder Ownership Report, the median founding team holds about 56% of the company after a priced seed round and about 36% by Series A (Carta). That is more than twenty percentage points gone in a single step, the steepest drop in a company’s life. The most common priced round sells between 20% and 24% of the company.

Two numbers are worth remembering. Founders give up roughly 20 points of ownership per early round, and the option pool is a large, negotiable part of that. The institutional standard also protects the downside: a 1x non-participating liquidation preference now appears in the large majority of clean priced rounds, so a term sheet proposing participating preferred or a full ratchet is off-market and worth pushing back on.

There is one number the region does not have. No published dilution benchmark exists for Gulf founders specifically, which means many anchor to whatever a single investor proposes rather than to a market standard. The fix is not a regional figure that nobody can source. It is to anchor to the global standard on round size, pool, and protective terms and negotiate from there. I set that out with the numbers in the GCC founder dilution and term-sheet benchmark.

The three levers that actually move your final number

Once you can see the three surprises, three levers do most of the work.

The pool. Negotiate the size and, harder but more valuable, the pre-versus-post-money treatment. A smaller pool sized to an actual twelve-month hiring plan, rather than a round 15%, keeps points in your column.

The SAFE stack. Model every outstanding SAFE at the round price before you sign the priced term sheet, not after. If you are still raising on SAFEs, know your fully diluted ownership after conversion before you add another instrument, because each one is a pre-commitment against a cap table that does not exist yet.

The round size. Raising more than the plan needs is dilution you chose. Size the round to the next milestone plus a margin, not to the largest number an investor will offer.

None of this is exotic. It is the difference between walking into the negotiation with your own fully diluted model and walking in with the investor’s headline number. If you want the specific structures that turn into problems, our Cap Table Red Flags PDF is the checklist I use to pressure-test a table before a raise: the eight patterns that cost founders equity or stall diligence, and how to fix each one before an investor asks. It is the fastest way to find out whether your own cap table is carrying any of them.

Model it before you sign, not after

The founder who thought he owned 62% was not wrong about his company. He was wrong about his arithmetic, and he found out at the worst possible time, mid-negotiation, when the emotional cost of re-cutting the deal is highest and his negotiating position is weakest.

The whole point of running the math early is that every one of these levers is negotiable while the term sheet is still a draft and immovable once it is signed. A fully diluted model that shows your ownership after the pool, after the SAFEs, and after the round is not a nice-to-have. It is the document that tells you whether the deal in front of you is the deal you think it is.

If you are not sure where your own numbers sit, the free Investor Readiness Scorecard is a quick way to see which parts of your raise are ready and which will surface in diligence. And if the model, the cap-table scenario, and the founder narrative all need building properly before you go out, that is the work of our Investor Readiness Sprint: a fixed-fee build, AED 25,000, delivered in two to three weeks from complete intake, that produces the deck, the management-input operating model, and one post-raise cap-table scenario so you walk into the round owning your own math. The Investor Readiness Sprint does not raise the money or run the process. It makes sure that when the term sheet lands, the number you keep is one you chose in advance, not one you discover at close.