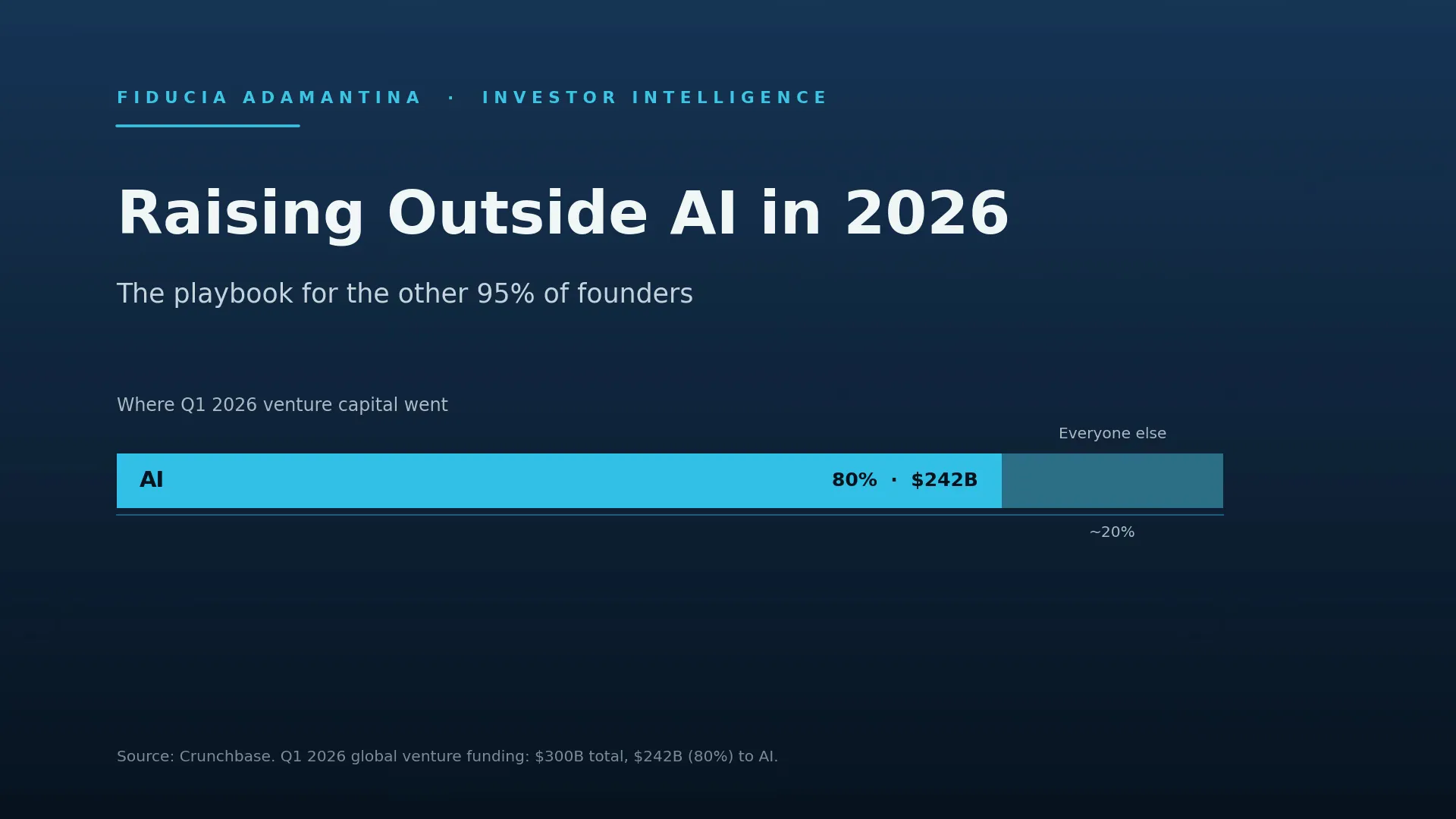

Global venture capital had its biggest quarter on record in early 2026. Roughly $300 billion went into startups in Q1 alone, the largest three months the asset class has ever seen, according to Crunchbase. If you are raising right now and that number makes you feel like you are doing something wrong, read the next line slowly. About $242 billion of it, four dollars in every five, went to artificial intelligence companies.

That is the whole story of this market in two sentences. Capital is at an all-time high, and almost none of it is looking for you.

Record funding and an empty inbox are both true

Most fundraising advice for 2026 starts from the headline and stops there. It tells founders capital is flowing and to go get some. That advice is useless if you are building anything other than a frontier model, because the average of a bifurcated market describes no one in it.

Here is the split without the spin. Four of the five largest venture rounds in history closed in that single quarter. OpenAI, Anthropic, xAI and Waymo between them took in about $188 billion, close to two-thirds of the entire global total (Crunchbase). Strip those handful of deals out and the picture for everyone else looks nothing like a record. The roughly 20% of capital that was not chasing AI got divided among thousands of companies across every other sector on earth.

So when a fund tells you it is “focused on AI right now,” it is not a brush-off. It is an accurate description of where the industry pointed its money. The problem is not that you are unfundable. The problem is that you are competing for a much smaller pool than the headline implies, against founders who have all read the same headline.

What March in MENA actually showed

The regional data made the same point more sharply. In March 2026, startups across the Middle East and North Africa raised a combined $48.3 million across just 17 deals, down 85% month-on-month and 62% year-on-year, per Wamda. Read on its own, that number looks like a collapse.

It was not. The region rebounded to around $150 million in April and closed the first quarter at $941 million (Wamda), with the UAE leading and fintech taking close to half of all capital. For context, MENA raised a record $7.5 billion across 2025. March was a timing and geopolitics story, founders holding announcements and investors reassessing exposure, not a structural exit from the region.

I point this out because founders raising outside AI tend to make one of two mistakes when they read a bad month. They either panic and take the first term sheet that appears, or they freeze and wait for the market to “come back.” Both are expensive. The capital is there. It is slower, more selective, and it is asking harder questions than it did in 2021. That is a different problem from scarcity, and it has a different answer.

If you are not an AI company, four things change your odds

In our practice I have watched profitable, well-run companies struggle to raise in this market next to weaker AI-adjacent stories that closed in weeks. It is genuinely unfair. It is also the market you have. The founders who get funded in it are not the ones who complain that the game changed. They are the ones who adjusted to the four things that now decide a non-AI raise.

A credible path to profitability beats a growth story. The 2026 venture outlook is blunt about this. Outside AI, investors want a clear route to profitability, stronger unit economics, and real traction before they commit, a consensus echoed across the year’s outlooks from the Harvard Law School Forum on Corporate Governance to Wellington Management. Growth alone no longer clears the bar. If your model only works with the next round assumed, you are asking an investor to underwrite a bet they now expect you to have de-risked yourself. Show them the month you stop needing them.

Revenue quality decides your multiple. Not all revenue is read the same way in a tight market. Recurring, contracted, high-retention revenue is now worth far more to an investor than the same top-line number built on one-off projects or a concentrated handful of customers. Before you raise, know which of your revenue an investor will actually credit, and understand how a non-AI business gets valued when the froth is gone. The mechanics of that are worth reading properly; our piece on how mergers and acquisitions valuation works applies directly to how a fundraise is priced too.

Right-size the round to the market you are actually in. The single most common mistake I see is a founder anchoring their raise to 2021 round sizes and 2021 valuations. A round that is too large for your traction does two things at once: it stalls, because the metrics do not support it, and it signals that you are not reading the room. A smaller, cleanly-justified round that gets you to a real milestone is far more fundable than an ambitious one that sits open for nine months and quietly kills your momentum. Scarcity rewards precision.

Widen the definition of capital. Venture is one source, and in 2026 it is the one most captured by AI. It is not the only one. Regional private equity, family offices, strategic investors and revenue-based structures are all active for profitable, non-AI businesses, and several are specifically looking outside the AI trade for exactly the durable cash flows you may already have. Gulf-based PE in particular is deploying into founder-led companies that would struggle to get a generalist VC meeting; if that is a fit, our overview of the region’s private equity firms is a sensible starting point. The founders who raise well in this market run a wider process than “20 VC intros.”

What “investor-ready” means when capital is scarce

Every one of those four adjustments assumes something most founders skip: that you know, before you go out, exactly how an investor will read your company. In a hot market you can be sloppy about this and get away with it, because capital is forgiving when it is abundant. In 2026 it is not. The gap between a founder who is investor-ready and one who merely thinks they are is the difference between a raise that closes and one that teaches you an expensive lesson over six months.

Being investor-ready in this market means your profitability path is evidenced rather than asserted, your revenue is presented the way a diligent investor will actually score it, your round is sized to what your numbers support, and your target list reflects who is genuinely funding companies like yours right now. None of that is glamorous. All of it is controllable, and getting those four right before you go out is the core of what an Investor Readiness Sprint does.

If you want a fast, honest read on where you stand against what investors are actually funding this year, Fiducia Adamantina’s Investor Readiness Scorecard is the place to start. And our free GCC Fundraising Data Snapshot gives you the current regional figures broken down by stage and sector, so you are pricing your raise against real numbers rather than the headline. Both are free, and both are built for exactly the founder this article is written for.

The honest close

The record-funding headline is not written for you, and pretending otherwise leads founders to raise the wrong round the wrong way at the worst possible time. The founders who get capital outside AI in 2026 are the ones who accept the market as it is, prove the things it now demands, and run a real process to find the capital that fits them.

That is the work an Investor Readiness Sprint exists to do. It is not a course or a readiness product, it is the paid first step of a raise: three weeks to build the profitability case, the revenue narrative, the right-sized round and the process design that a scarce, selective market requires, so that when you go out, you go out ready. From there the goal is the same as it has always been, the raise itself and the mandate that runs it to close. If you are planning to raise in the next six to twelve months and you are not an AI company, that readiness is not optional this year. It is the whole game.