A founder I worked with had a clean business and a messy table. Profitable, growing, a real Series A story. Then the cap table came out: a co-founder who left in year two still held 28 percent, two friends-and-family cheques had no paperwork beyond a WhatsApp thread, and a local sponsor from the original 2019 licence was still listed as a 51 percent shareholder. The term sheet conversation slowed to a stop while lawyers worked out who actually owned the company.

The cap table rarely kills a raise loudly. It does it quietly, in diligence, after the founder has already spent weeks selling the vision. By then the investor is not excited; they are nervous. This post is about the cap-table problems I see most often in MENA deals, why they differ from the ones a US-built checklist warns you about, and how to fix them before an investor ever asks.

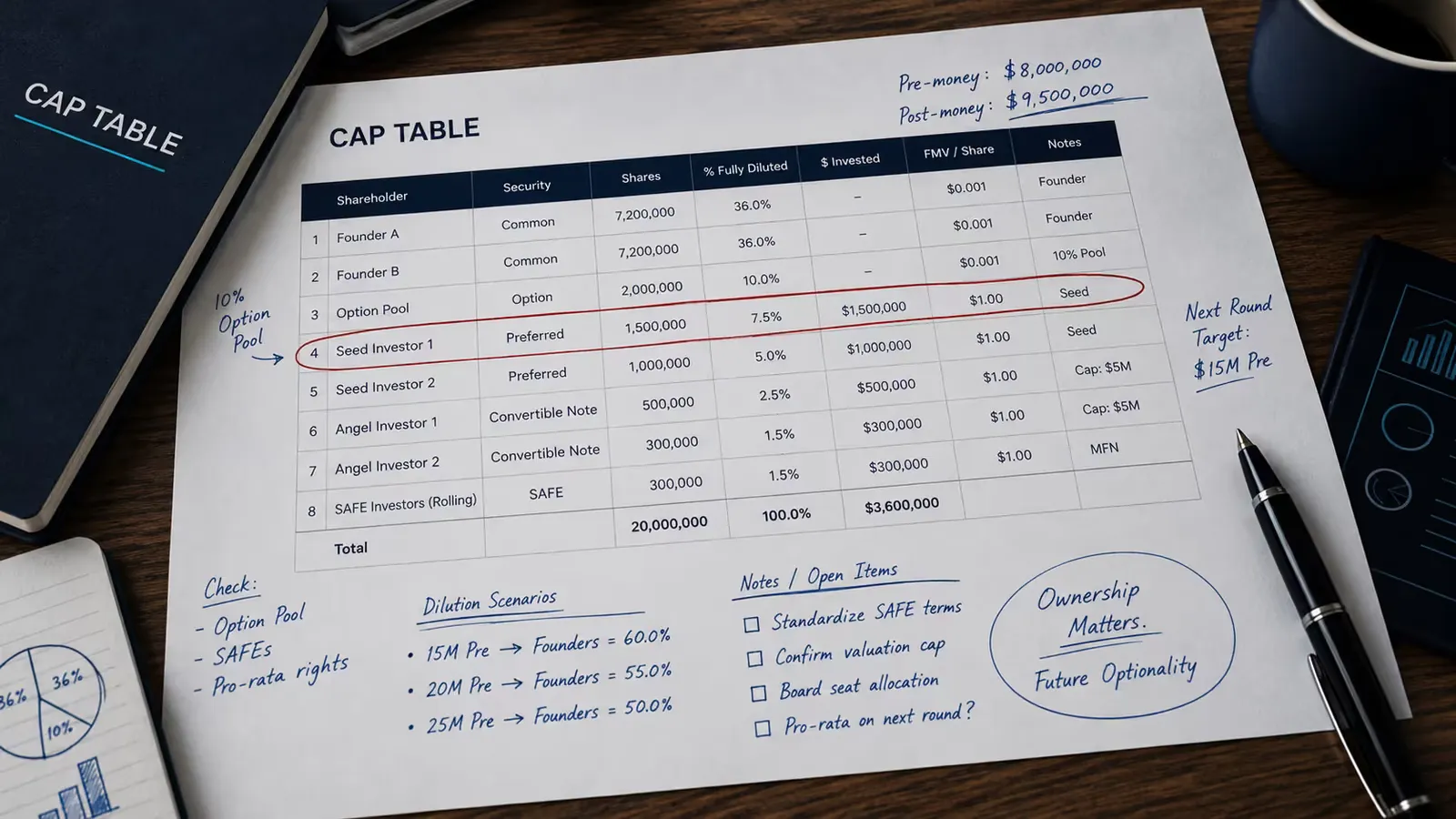

The cap table is the first document a serious investor opens

Founders treat the deck as the centre of the raise. Investors treat the cap table as the proof. The deck is the story; the cap table is whether the story holds up legally and whether there is enough equity left to make the deal worth doing.

When an investor opens it, they read two things at once: who owns the company and whether those people still add value, and whether the founder runs a tight ship. A cap table with undocumented holders, mystery percentages, and stale splits says the rest of the house is probably just as loose. It reframes every other number in the room.

The good news: cap-table problems are almost always fixable before a raise, and almost never fixable during one. The whole game is timing. If you are not sure which side of that line your table sits on, score yourself against the Investor Readiness Scorecard — the cap table is one of the readiness dimensions it checks, and it flags the structures a diligence team will question while there is still time to fix them quietly.

Red flag 1: dead equity, the co-founder who left but still owns 30 percent

The most common deal-killer I see is dead equity: a meaningful stake held by someone who no longer contributes. An early co-founder who walked after eighteen months. A “marketing advisor” from year one who has not answered an email since.

To a new investor this is not a loyalty question, it is a math problem. Every point held by someone inactive is a point not available to motivate the people building the company now, and not available to the investor. A team that has already given 30 percent to people who are gone looks like a team that will run out of equity to incentivise the next twenty hires.

The fix is rarely comfortable and almost always possible: vesting that should have existed can sometimes be negotiated retroactively, or a buyback at fair value clears the stake cleanly. Neither is quick, which is exactly why they belong in the months before a raise, not the weeks during one.

Red flag 2: the dormant local sponsor nobody cleaned up after 2021

This one is specific to the region and I see it constantly. Companies licensed on the UAE mainland before mid-2021 were usually structured with a UAE national holding 51 percent of the shares, with side agreements assigning real economic ownership back to the founder. It was the standard workaround for a decade.

Then the law changed. Federal Decree-Law No. 26 of 2020 removed the 51 percent Emirati-ownership requirement for most mainland activities, effective 1 June 2021, so founders have been able to restructure to full foreign ownership for years. Many never did. The business kept running, the side agreement kept sitting in a drawer, and the official register still shows a sponsor owning a controlling stake.

An international investor running diligence does not see a harmless legacy arrangement. They see a third party with 51 percent of the company on paper, held together by a side letter of uncertain enforceability. That is a structural risk most institutional funds will not underwrite. The cleanup, converting to full foreign ownership and aligning the share register with reality, is administrative once started, but it runs through licensing authorities on their timeline, not yours. Start it the moment a raise is on the horizon.

Red flag 3: family shareholders with veto rights

Many regional companies were seeded by family money, and the equity that came with it often carried more control than the cash justified. An uncle who put in the first 200,000 dollars and took 20 percent and a board seat. A family holding company that owns a quarter of the business and, buried in the articles, holds a veto over future share issuance.

A founder can live with this for years. An investor cannot. If a family shareholder can block the very share issuance the new round requires, the investor is not buying into the founder’s decision, they are buying into a negotiation with a third party they have never met. Deals stall here more often than founders expect.

The work is to map every control right attached to every shareholder long before the raise, not just the ownership percentages: veto rights, board seats, pre-emption clauses, drag and tag provisions. Where a family stake carries control that no longer fits the company’s stage, that conversation needs to happen inside the family, on a relaxed timeline, well before an investor asks why it has not.

Red flag 4: friends-and-family convertibles with no paper trail

Early money in this region often arrives informally. A cousin wires 50,000 dollars on the understanding that it converts to equity “at the next round.” A former colleague hands over a cheque against a one-paragraph email. Nobody signs a proper instrument because everyone trusts each other.

That trust becomes a liability the moment a real investor arrives. An undocumented convertible is an unknown claim: how much equity does that 50,000 dollars convert into, at what valuation, with what cap? If the answer lives in someone’s memory rather than a signed document, the founder’s fully diluted ownership is unknowable, and an unknowable cap table is one an institutional investor will not price.

Every dirham or dollar that came in against a promise of future equity needs a proper instrument behind it: a convertible note or a SAFE with a stated cap, discount, and conversion mechanics, signed by both sides. Papering these after the fact is harder than doing it upfront, but far easier before a term sheet exists than after.

Red flag 5: equity scattered across free-zone and mainland entities

The structural complication unique to this market is multi-entity sprawl. A DIFC or ADGM holding entity, a mainland LLC for the business that needs to invoice locally, a free-zone entity in another emirate for a licensing reason, and perhaps an offshore company someone advised setting up early. Five years in, equity, IP, and revenue are spread across four entities with no clean parent.

An investor wants to buy shares in one company that owns everything that matters: the IP, the contracts, the revenue, the team. When those assets sit in separate entities with no holding structure tying them together, the first diligence question is which company they are actually investing in, and the answer is usually “it’s complicated.” Complicated is the word that delays term sheets.

The remedy is a clean holding structure, operating entities sitting under a single parent that investors buy into, with IP and key contracts assigned to the right entity. This is the most involved fix on the list. It touches tax, licensing, and sometimes employee visas, and it cannot be done in the four weeks before a close. It is the clearest argument for treating cap-table cleanup as a months-out project, not a diligence scramble.

How to clean a cap table before investors look, not during diligence

The pattern across all five is the same: each is fixable on a calm timeline and almost unfixable on a deal timeline. A buyback negotiated when no investor is watching is a fair-value transaction; the same buyback mid-raise, when the departing shareholder knows you need their signature to close, is a hostage situation. Timing is the entire difference between a clean fix and a discounted one.

The sequence before or alongside an Investor Readiness Sprint is straightforward. Build a true fully diluted cap table, including every undocumented claim, first. Open the dead-equity conversations early because they take longest. Run legal cleanup, sponsor conversion, holding-structure work, and convertible documentation through the appropriate advisers on their clock. Map every control right, not just every percentage. The Sprint can model the current and post-raise positions and flag open issues; it does not execute the legal cleanup.

To make the first pass easier, we have put the full list of cap-table problems that derail MENA raises, with the cleanup approach for each, into a single reference: our Cap Table Red Flags PDF. It covers the five above plus the documentation and option-pool issues in nearly every regional deal, built to be read with your own share register open beside it.

What a clean cap table actually signals

A clean cap table does more than survive diligence. It tells an investor the founder runs a disciplined company, that there are no surprises in the documents, and that the equity left in the business is enough to make the deal and motivate the team through to exit. That signal raises the quality of every conversation that follows.

Investors test four things before they wire: the cap table, the financial model, the narrative, and the operating data. The fastest way to see where you stand is our Investor Readiness Scorecard, a fifteen-minute self-assessment that scores each dimension and flags the gaps to close before you approach investors. The Cap Table Red Flags PDF sits in the same resource library, so you can score the equity dimension and pull the cleanup reference in one pass.

If the Scorecard shows cap-table or structure problems, separate modelling from remediation. The Investor Readiness Sprint can model the current and post-raise positions, identify open issues, and rebuild the pitch materials. Legal cleanup, data-room work, and confirmation that the structure is clean remain outside the AED 25,000 fixed scope. The product stands alone; paid fees are eligible for the optional 90-day raise-mandate credit.

Founders do not lose deals because their cap table is complicated. Every growing company’s cap table is complicated. They lose deals because the complications are unresolved when the investor looks. Resolve them first, and the table stops being the thing the deal dies on.