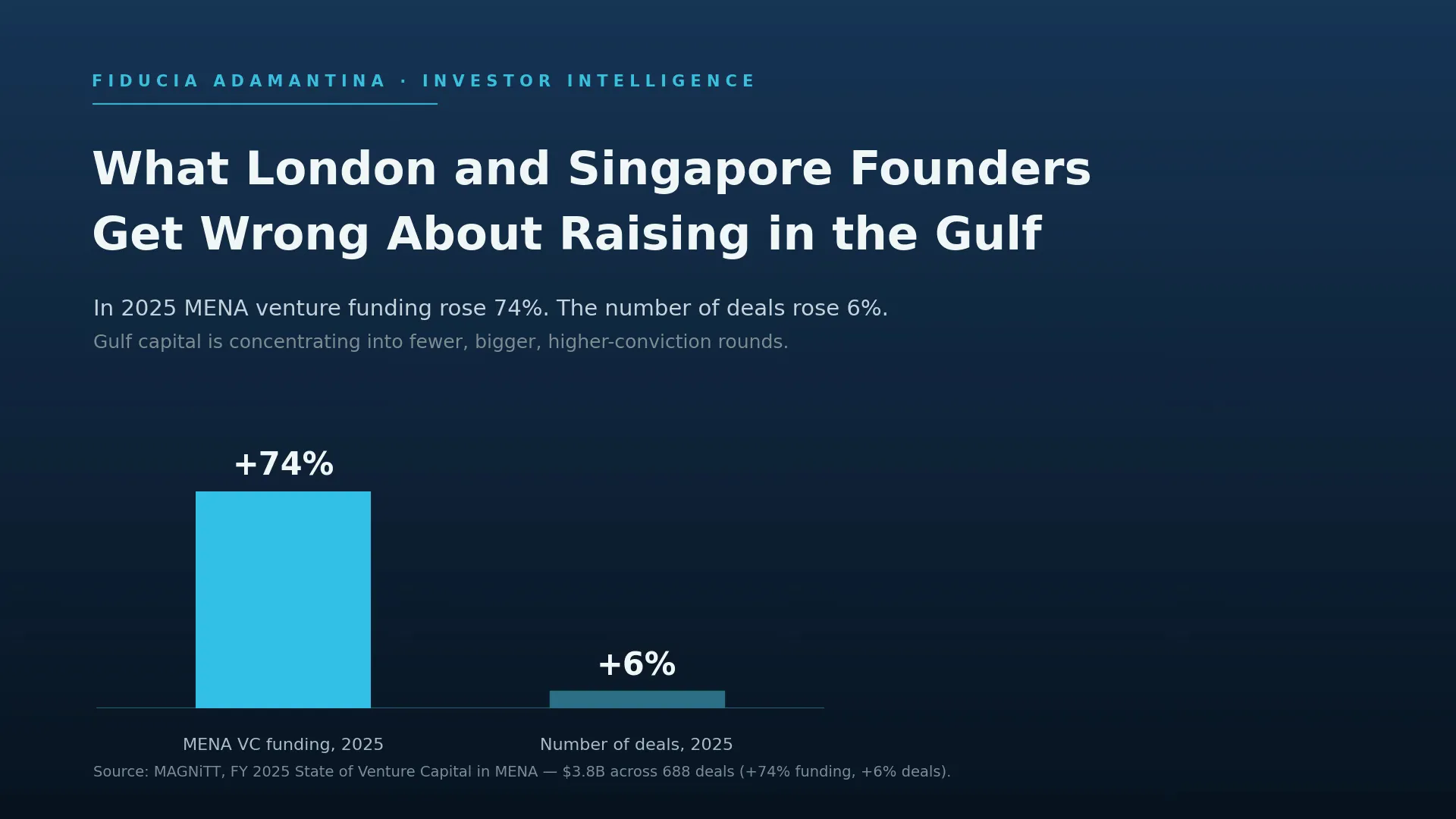

In 2025, venture funding across MENA grew 74 percent to $3.8 billion. The number of deals that absorbed it grew 6 percent (MAGNiTT, FY 2025 State of Venture Capital in MENA). That gap is the single most important fact an international founder needs before raising in the Gulf, and almost none of them have it.

More money flowing into barely more companies means capital is concentrating into fewer, larger, higher-conviction rounds. The first quarter of 2026 made the point sharper: deal activity fell to its weakest quarterly level in five years while average cheque sizes hit new highs, with regional funding around $941 million for the quarter. The Gulf is not writing more cheques. It is writing bigger ones, to founders it has already decided to believe in.

A founder who raised in London or Singapore is trained for the opposite market, one where volume, speed, and a sharp narrative carry a process forward. I work with founders from both cities who land in the UAE assuming the playbook that worked at home will travel. It rarely does. The mechanics of a Gulf raise differ enough that a deck which closed a round in Europe can draw a room of polite nods and no second meeting, and the founder leaves with no idea what went wrong.

Here is what they are usually missing.

Mistake 1: Assuming Gulf investors behave like London or Singapore VCs

In a London seed round, a founder can run a competitive process across thirty funds, create urgency, and close on momentum. The institutional VC machine there rewards speed and optionality.

Gulf capital is structured differently. A large share of the region’s money sits with sovereign-backed funds, corporate investment arms, and family offices. These are pools of capital that are patient, relationship-led, and far less interested in a fear-of-missing-out sprint. When a founder tries to manufacture urgency with this kind of investor, it reads as pressure, and pressure reads as risk.

The 2025 concentration data is the tell. When capital flows to fewer, larger rounds, it means investors are backing conviction, not spreading small bets across a portfolio to see what sticks. You are not being scored on how hot your round is. You are being scored on whether this specific investor believes in you enough to write a meaningful cheque and stand behind it.

That changes how you run the process. Fewer conversations, deeper ones. Less theatre, more substance.

Mistake 2: Treating relationship-building as a formality, not the work

The most expensive assumption I see international founders make is that the relationship is something you do around the raise. In the Gulf, the relationship is the raise.

A first meeting is almost never a deal meeting. It is an introduction. Trust in this market is built in person, over more time than a founder optimising for a tight raise window expects to spend. Founders who fly in for a three-day investor trip, take eight meetings, and fly out wondering why nothing converted have misread the timeline by a wide margin.

This is not inefficiency. It is how sophisticated, long-horizon capital protects itself. A family office deploying its own principal’s wealth has no fund clock forcing it to deploy by year-end. It can wait until it is sure. Your job is to start earlier than feels necessary and let the relationship mature before you need the money.

The founders who raise well here treat their first Gulf trip as the beginning of a six-to-twelve-month arc, not a closing sprint.

Mistake 3: Pitching a global story when the room wants a regional one

A London or Singapore deck usually leads with a global market and a global ambition. That framing wins at home. In the Gulf it often lands flat, because it answers a question the investor in front of you is not primarily asking.

Gulf investors, and the governments whose diversification agendas shape their mandates, care about what you will build in the region. Will you create jobs here? Bring technology or capability into the local market? Anchor operations in Riyadh or Abu Dhabi rather than treating the Gulf as an ATM for a business run from elsewhere? Industry reporting through 2025 has been consistent that capital is increasingly directed toward companies with genuine regional roots.

This does not mean abandoning your global story. It means leading with the regional one. The opportunity narrative that wins in Dubai puts the Gulf at the centre of the plan, not in a footnote on slide fourteen. If your honest answer is that the region is just a funding source and you have no intention of building here, sophisticated investors will sense it, and that is often the quiet reason a strong-looking deck stalls.

This is also where deck mechanics matter. The way you frame market size, regulatory awareness, and use of funds has to be rebuilt for this audience, a point I cover in detail in seven pitch deck mistakes that turn off GCC investors.

Mistake 4: Ignoring the family office channel entirely

Most international founders arrive with a mental map of the local VC funds and stop there. They miss the channel that has become one of the most active sources of early-stage capital in the region: the family office.

Gulf family offices have moved well beyond wealth preservation. Through 2025 they have increasingly behaved like direct venture investors, backing technology, fintech, and other high-growth companies straight off their own balance sheets (World Economic Forum, 2025). For a founder, this is patient capital with real strategic reach across the region, and a relationship that, once earned, tends to compound into introductions and follow-on support.

But family offices are not on a directory you can mail-merge. They are reached through trusted introductions, and they evaluate founders on judgement and alignment as much as on metrics. A founder who only works the named-fund channel is competing in the most crowded part of the market while ignoring the part where conviction capital actually concentrates.

Mistake 5: Trying to raise the Gulf without standing in it

The last mistake is the one founders most want to avoid hearing, because it is the most inconvenient: you generally cannot raise the Gulf from a hotel room.

Investors here want to see commitment to the region before they commit capital to you. That does not always mean a full relocation. It can mean a properly structured local entity, a regional hire, a co-founder spending real time on the ground, or a credible advisor with genuine relationships who is actively involved rather than a name on a slide. What it cannot mean is a founder who treats the Gulf as a remote ATM and expects the region’s most selective investors not to notice.

Choosing the right footprint (DIFC versus ADGM, what the ownership rules actually require, how to sequence the first ninety days) is a real piece of work in itself. I walk through the operational version of that decision in raising in the UAE as a foreign founder.

What changes when you localise the raise

None of these mistakes is fatal. Every one is fixable with preparation, and the founders who fix them are not better-pitched. They are better-prepared for this market specifically.

Start with the deck, because it is the artefact every other mistake shows up in. A deck built for London investors and a deck built for Gulf investors share a skeleton but differ in emphasis: regional market sizing, explicit unit economics, regulatory awareness as a trust signal, and a use-of-funds story that shows you intend to build here. Our free Pre-Meeting Investor Checklist is built around exactly what investors in this region expect to see walking into a first meeting, and it is the fastest way to pressure-test whether your deck and materials are speaking their language or your home market’s. Beyond the deck, the free Investor Readiness Scorecard gives you a fifteen-minute read on where the rest of your raise stands across legal structure, financial clarity, materials, and positioning, and it surfaces the gaps a Gulf investor will find before they find them. It is also worth understanding what GCC investors actually look for beyond revenue, because the scoring criteria are not the ones most international founders assume.

The deeper point is that a Gulf raise is not your home raise with different faces in the room. It is a different process with a different rhythm, a different set of channels, and a different definition of what makes a founder credible. Doing that rebuild deliberately, before the first serious meeting rather than after it, is the work the Investor Readiness Sprint exists to compress. Treat the raise that way and the blank stares stop.

Get investor-ready before you book the flights

The most common version of this story is a founder who flew in, took the meetings, and only afterward discovered which of the five mistakes had been costing them. That is an expensive way to learn it.

The better sequence is to separate materials gaps from company gaps before the first serious conversation. The Investor Readiness Sprint rebuilds the defined deck, model, cap-table scenario, and narrative for AED 25,000 in 2–3 weeks from complete intake. It does not build the data room, validate the market, or repair legal, accounting, traction, or governance issues. Those prerequisites remain with management and the relevant specialists.

Start with the Investor Readiness Scorecard. If it shows you are closer than you feared, good. If it shows materials and presentation gaps, the Sprint may fit. If it shows company-level blockers, resolve those before treating a materials build as the answer.