Saudi Arabia pulled in $1.72 billion of venture capital in 2025, up 145 percent on the year across 257 deals, and took more than half of every dollar invested into MENA startups, according to MAGNiTT. It was the Kingdom’s strongest year since 2018 and its third running atop the region. Then the first quarter of 2026 arrived, and the same data houses reported a sharp regional pullback.

Both are true at once, and a founder reading only one will get the decision wrong. The structural story and the cyclical story point in different directions this year. This is the Saudi conversation I have most often in our practice right now: what has actually changed for a Series A founder in the Kingdom, where the capital really comes from in 2026, and why raising in Riyadh is no longer the same decision as raising in Dubai.

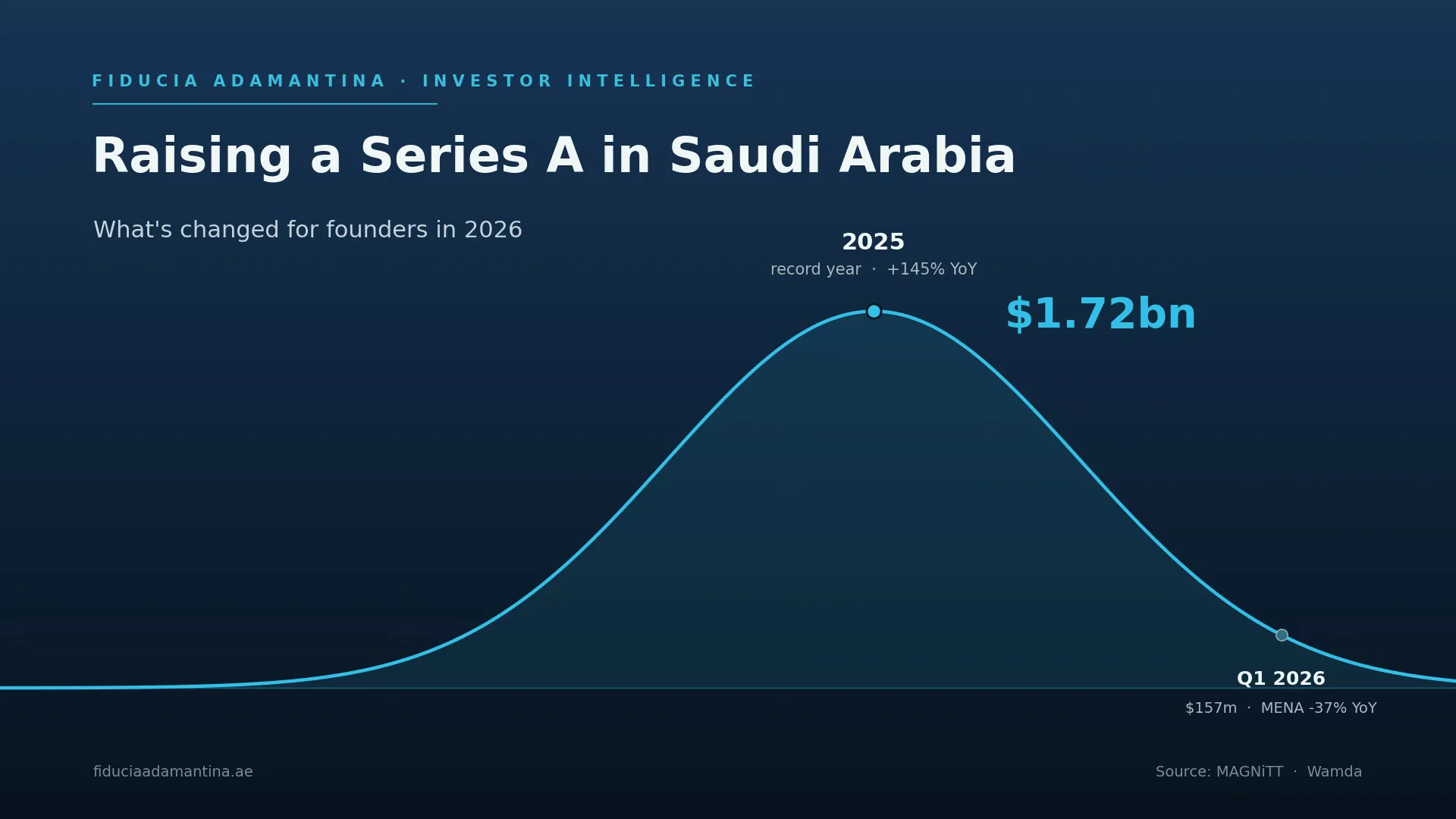

Read both numbers: the record year and the cooler quarter

The 2025 figure is the one that gets quoted. The 2026 figure is the one that should shape your timing.

Across MENA, startup funding slipped to $941 million in the first quarter of 2026, down 37 percent year on year amid heightened regional risk, on Wamda’s numbers. Saudi Arabia took $156.7 million of that across 57 deals, second behind the UAE for the quarter. Set against a $1.72 billion full year, that is a market that has cooled and broadened at the same time.

I tell founders to separate the two signals. The structural rise is durable: policy-driven, sovereign-funded, and not about to reverse on one soft quarter. The cyclical softness is real too, and it changes how a 2026 raise behaves on the ground. Cheques are still being written, but committees are slower, diligence deeper, and the bar for a first meeting higher than the 2024 and 2025 headlines suggest. Plan for the structural opportunity; prepare for the cyclical reality.

Vision 2030 did not just add capital, it changed who controls it

The biggest shift since the older guides were written is where the money originates. A decade ago, raising in Saudi Arabia meant a thin layer of private money and a lot of family capital. Today a large share of the supply traces back, directly or one step removed, to the state.

Two institutions explain most of it. Jada, the Public Investment Fund’s fund-of-funds, was set up with SAR 4 billion and has committed billions across dozens of funds rather than backing startups directly. Its job is to seed the local VC layer. Sanabil, also wholly owned by PIF, deploys around $3 billion a year into venture, growth, and small buyouts, and runs accelerator programmes alongside the cheques.

The practical consequence for a founder is not that you pitch a sovereign fund; you rarely do at Series A. It is that the venture funds you do pitch are often backed by Jada or Sanabil, so their mandates carry a Vision 2030 flavour: localisation, sector priorities, job creation, and a preference for companies committed to building in the Kingdom rather than treating it as a cash machine. That lineage explains the questions a fund asks. The capital is patient and strategic because its backers are.

The VC field in 2026: bigger cheques, sharper mandates, less patience for tourists

The local fund layer has matured fast. The largest manager, STV, runs an $800 million fund and writes cheques from roughly $5 million to $50 million across Series A and growth, and in 2025 it added smaller AI-focused and venture-debt vehicles on top. A market that once had a handful of credible Series A leads now has a genuine field of them, each with a stated focus.

That maturity cuts both ways. The cheques are larger and the mechanics familiar to anyone who has raised in London or Singapore, but the mandates are sharper, and patience for what regional investors privately call “tourists” — founders who arrive for a season, raise, and leave — is thin. The most common mistake I watch international founders make is treating Saudi VCs as interchangeable and sending the same note to twenty of them. Stage, sector, and cheque size are stated publicly by most of these funds. Match yours to theirs before you reach out.

Some founders should also ask whether a raise is the right move at all. For a profitable regional business, a strategic sale can be a cleaner path to liquidity than a Series A, and the two processes look very different. If that question is live for you, our walk-through of the M&A process sets the comparison out. Most founders reading this will raise; some should not, and it pays to know which first.

Riyadh vs Dubai: the RHQ rule rewrote the basing decision

For years the default was simple: base in Dubai, sell into Saudi Arabia. The DIFC and ADGM ecosystems were deeper, and Riyadh was a market you flew into. In 2024 the Kingdom changed the maths.

Since 1 January 2024, a company must base its regional headquarters inside Saudi Arabia to be eligible for Saudi government contracts. The programme pairs that with a thirty-year exemption from corporate income and withholding tax on qualifying RHQ activity, and has already pulled in more than 540 multinationals, most landing in Riyadh. It was designed for large corporates, not startups, but the gravitational pull reaches founders too.

If any meaningful slice of your revenue will come from Saudi government or government-linked buyers, and in the sectors the state is prioritising much of it will, then a Dubai-only structure now carries a cost it did not carry in 2022. The question is no longer “Riyadh or Dubai” as a lifestyle choice. It is where your customers and your capital actually sit, and whether your structure lets you sell to both. For the UAE side of that decision, our step-by-step guide to raising in the UAE covers the entity and regulator questions in the same depth. Increasingly the right answer for a Gulf-wide Series A company is a deliberate presence in both.

What Saudi investors actually want to see before a Series A

Regulatory progress counts as traction. In fintech, healthtech, and other licensed sectors, a SAMA sandbox place or an SFDA pathway reads as a real milestone, sometimes more convincing than another month of user growth. Document it. Bilingual materials are close to mandatory: a deck and model in both Arabic and English signal you are serious, and substantive diligence is often handled in Arabic. And local commitment is scrutinised: investors backed by state-aligned capital want to see you intend to build in the Kingdom, not extract from it.

Underneath the regional specifics, investors still test the cap table, financial model, narrative, and data room. The Investor Readiness Framework helps diagnose those areas. The Investor Readiness Sprint can rebuild the defined pitch materials and model a cap-table scenario; it does not clean the legal structure or build the data room.

Where the 2026 capital is concentrating

In a cooler market, sector matters more: capital narrows toward the themes the state’s funds favour most.

Fintech remains the centre of gravity: it took 46 percent of MENA investment in the first quarter of 2026. Around it sit the sectors Vision 2030 has prioritised and state-aligned funds steer toward: healthtech, logistics and mobility, e-commerce enablement, and increasingly applied AI. A founder building squarely in one of those finds the 2026 market far warmer than the headline pullback implies. One outside them needs a sharper story about why a Saudi investor should care.

This is where current data earns its keep, and where a 2022 article will mislead you. We keep the regional picture we use in our own practice in a single reference, the GCC Fundraising Snapshot: sector splits, regional cheque sizes, and the year-on-year direction of travel. It sits alongside the Investor Readiness Scorecard in our resource library, the right way to pressure-test whether your sector and timing line up before you commit to them.

Timing a Series A into the Saudi cycle

Capital conversations in the Gulf cluster in two windows each year, roughly September to November and February to April, anchored by the large autumn gatherings in Riyadh and Dubai. The implication for 2026 is specific. A soft first quarter does not mean you wait for the market to recover. It means you use the quiet to prepare, so you move into the autumn window with your structure, cap table, materials, and warm-introduction map already done.

Founders who run it the other way, starting the raise and assembling materials under pressure, discover four months in that a round they expected to close in twelve weeks is still open. The cooler the market, the more brutal that lesson. Preparation is the variable you control; the cycle is not.

Get investor-ready before you approach

Saudi Arabia in 2026 is a more serious market than most guides describe and more demanding than the 2025 headlines suggest. The capital is deep, increasingly institutional, and concentrated in the sectors the state has chosen, and the bar to earn it has risen in step. A founder who shows up prepared, with a clean structure and a story that survives diligence, meets a market ready to back them. One who shows up to figure it out in real time meets a market that has seen that film and is in no hurry.

The fastest way to find out where you stand is our Investor Readiness Scorecard, a short self-assessment that scores your cap table, model, narrative, and data room and flags the gaps to close before a single Saudi investor sees your name. The GCC Fundraising Snapshot sits in the same library, so you can size the opportunity and score your readiness in one pass.

When the Scorecard identifies materials and presentation gaps, the Investor Readiness Sprint can rebuild the defined deck, model, cap-table scenario, and founder narrative for AED 25,000 in 2–3 weeks from complete intake. It is independently buyable and does not include data-room work or raise execution. Paid fees are eligible for the optional 90-day raise-mandate credit.

Saudi Arabia is where much of the region’s capital now lives. Get ready before you ask for it.