“A buyer sent me a 200-line document request and I’d never seen half the items before.” I hear that from founders already weeks into a sale, not at the start of one. The early calls went well. Then the buyer’s diligence team sends the request list, and it asks for things no investor ever did: a quality-of-earnings pack, a customer-concentration breakdown by revenue, change-of-control language in every material contract. The founder reads it as a paperwork problem. It is not. It is the opening move in a price negotiation, and the founder is already a step behind.

Sell-side due diligence is the buyer’s process of verifying what they are about to own. The mistake is treating it as an exam you sit when the request list arrives. By then you are answering under exclusivity, your alternatives gone quiet, the buyer holding the clock. The work that protects your price happens before the list ever lands. This post is about what buyer scrutiny tests that investor diligence never did, and how to prepare early enough that nothing in the room costs you money.

Investor diligence asks “is this worth backing?” Buyer diligence asks “is this worth owning without you?”

Founders who have raised think they know diligence. Buyer diligence is a different test with a different motive.

An investor buys a minority stake and a story about the future. They underwrite upside, and they tolerate gaps because they are betting on growth and on you to deliver it. A buyer purchases the whole thing and inherits every liability inside it. They underwrite downside. Every gap they find is either a reason to pay less or a risk to push onto you through the deal structure.

That changes what gets examined. The raise-side data room I describe in how to prepare a data room that passes investor due diligence is the foundation, and a founder who has built one is ahead. But buyer diligence adds a layer investors rarely touch: the durability of your earnings, your dependence on a handful of customers, whether your contracts survive a change of ownership, and whether the business runs without you in the room. Those are the items that turn a 200-line list into a renegotiation.

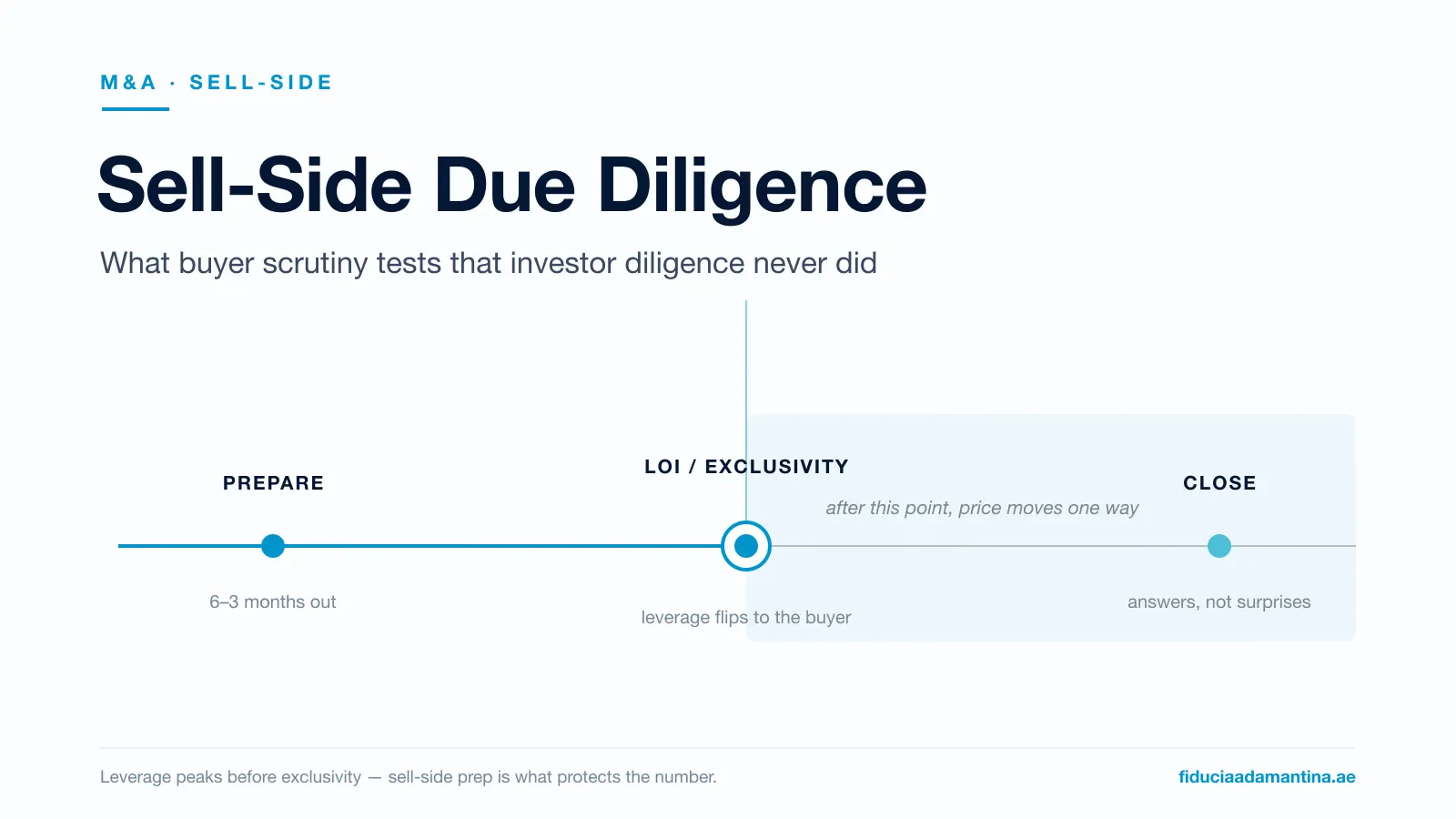

Where sell-side due diligence sits in the deal

Diligence is not a single stage you reach. It runs underneath the whole M&A process and tightens sharply once you sign a letter of intent and grant exclusivity.

That is the whole argument for preparing early. Before exclusivity you hold leverage: other conversations, the option to walk, a buyer who still has to win you. After it, the leverage flips, and a diligence list lets the buyer reopen price every time something surfaces dirty. The founders who hold their number ran the buyer’s analysis on themselves months earlier, when a problem was still cheap to fix and private.

Quality of earnings: the test your management accounts have never faced

The first thing a serious buyer commissions is a quality-of-earnings analysis. It is not an audit. An audit asks whether your numbers are accurate. A quality-of-earnings review asks whether your profit is real, repeatable, and transferable: how much of last year’s EBITDA is recurring versus one-off, which add-backs survive scrutiny, and what normalised earnings look like once owner discretionary costs and related-party items come out.

This is where founder numbers most often slip. A management P&L that was good enough to run the business, and good enough for an investor’s growth story, can still come apart under a buyer’s analyst, because the analyst is not testing the trajectory. They are testing the base. If the cleaned-up number is lower than the one your asking price was built on, diligence is where the two get introduced, and the price moves toward the lower one.

The preparation is to run that analysis before the buyer does. A growing number of sellers now commission their own sell-side quality-of-earnings review so nothing surfaces for the first time in the buyer’s process. Advisers estimate only about half of lower-middle-market, founder-led businesses bother, and they push the ones who do to start three to six months ahead, precisely to avoid surprises later in buyer diligence (Middle Market Growth, Fall 2025). Run early, the review often works in your favour, documenting legitimate add-backs that defend a higher number rather than a lower one. You do not need a formal report to begin. You need to know which of your earnings survive normalisation, and to document every adjustment before someone else makes it for you.

Customer concentration: the number a buyer fixates on that an investor shrugged at

To an investor, a marquee customer worth 30% of revenue can read as validation. To a buyer it reads as a single point of failure they are about to own.

Buyers start asking hard questions when one customer, or a small cluster, runs past 20 to 25% of revenue. The buyer is picturing that account leaving after you do, taking a quarter of the business with it. The pricing response is predictable: less cash at closing, a holdback tied to those accounts renewing, an earnout that parks the risk back on your side of the table.

You cannot re-engineer your revenue base in the weeks before a sale. You can document the relationships, show contract length and renewal history, demonstrate that each account sits with the company rather than only with you, and broaden the base where there is still time. A founder who walks into diligence already holding that evidence controls the conversation. A founder asked for it cold confirms the buyer’s fear.

Contract assignability: the clauses that decide whether the deal even transfers

Here is an item almost no founder thinks about until a lawyer raises it: do your contracts survive the sale?

Many commercial agreements carry change-of-control or assignment clauses: some need the counterparty’s consent before the contract can transfer to a new owner, some let the counterparty walk away if control changes hands. If your largest customer contract, a key supplier agreement, or your office lease can be cancelled the moment you sell, the buyer is not acquiring what they think they are, and their lawyers find it in the first weeks.

The fix is unglamorous and entirely doable in advance. Read your material contracts for change-of-control and assignment language. Know which ones need consent, and where a relationship is strong, open quiet conversations early. Surfacing this yourself, with a plan, signals a well-run company. Having the buyer’s lawyer surface it first is a discount waiting to happen.

Key-person risk: can the business run without you in the room?

The hardest question in buyer diligence is not on any document list. It is whether the business works once you are gone.

Buyers probe it everywhere: the org chart, management meetings, whether they can speak to your second tier without you present. A company where the founder holds every key relationship, approves every meaningful decision, and carries the operating knowledge in their head is, to a buyer, a job they are being asked to buy rather than a business. The structural response is the one founders dread: a longer earnout, a longer lock-in, more of the price made contingent on you staying.

Building management depth is the highest-return preparation item here, and the one that takes longest, which is why it must start early. This is the same readiness discipline Fiducia Adamantina runs on the raise side through the Investor Readiness Sprint, where the work is making a company legible to an investor before it goes to market. On the sell side the goal is the mirror image: make the company independent of the founder before a buyer tests whether it is.

The GCC layer: multi-entity structures and the paper trail

If you are selling a business built in the GCC, buyer diligence adds a regional layer that generic checklists miss, because the corporate structure here does not look like Delaware.

Free-zone versus mainland status, the activities your trade licence actually permits, and how an offshore holding company connects to a local operating entity are all diligence items, not background. So is ownership history. Until recently most mainland companies needed a 51% Emirati shareholder; the UAE removed that requirement for most mainland activities under Federal Decree-Law No. 26 of 2020, effective 1 June 2021. Many founders restructured to full ownership and never cleaned up the trail: an old side agreement, a nominee arrangement, a former sponsor still sitting on a registry. A buyer’s lawyer finds these quickly.

Tax is now a live diligence question too. Since the UAE introduced corporate tax at 9% on profits above AED 375,000 for financial years starting on or after 1 June 2023, a buyer expects to see your corporate-tax registration and, where relevant, your VAT and economic-substance position. A company that is not registered, or whose structure was built for an older tax reality, is a flag a buyer will price.

It is worth seeing where you actually stand. The free Exit Readiness Scorecard scores your business across the same dimensions a buyer’s team will test, flags the issues that re-trade a price, and returns a readiness level in about fifteen minutes, while every gap is still cheap to close. For the exhaustive, document-by-document version, the M&A due diligence checklist lays out every item a buyer will pull and what each one costs when it surfaces dirty.

Build the answer before the question

Every item here is fixable quietly, on your own timeline, before a process starts. None of them is fixable gracefully once a buyer is holding a signed LOI and a deadline.

Treat preparation as two layers. The structural work is slow: earnings quality, customer concentration, management depth, and contract and corporate cleanup. Start it a year or more before you intend to sell. The Exit Readiness Sprint can diagnose the buyer issues, frame the adjusted earnings and value story, map the data-room gaps, and sequence a 90-day plan. It does not complete the structural work or build the underlying room.

A buyer’s request list is not a test of your patience. It is a pricing instrument. The founder who has already run that instrument on their own business meets diligence with answers instead of surprises, and answers are what hold a price from LOI to close.

If a sale is anywhere on your horizon, the cheapest move you can make is to find out now what a buyer would find. Book a strategy session and we will walk the buyer’s diligence list against your actual business, the same way an acquirer’s team will, except earlier and on your side of the table. Preparing this far ahead is the difference between selling on your terms and selling on theirs.