Most founders find out whether their business is sellable at the worst possible moment: after a buyer has already made an offer, when diligence starts pulling the company apart and the number on the term sheet quietly falls. By then it is too late to fix what the buyer found.

I meet founders who are years from selling and already anxious about it. They put the question to me the same way almost every time: “I’ll probably sell in a few years, but I have no idea whether I’m building something a buyer would actually pay for, or a job that falls apart the day I leave.” It is the right question, and it deserves an answer long before anyone is circling.

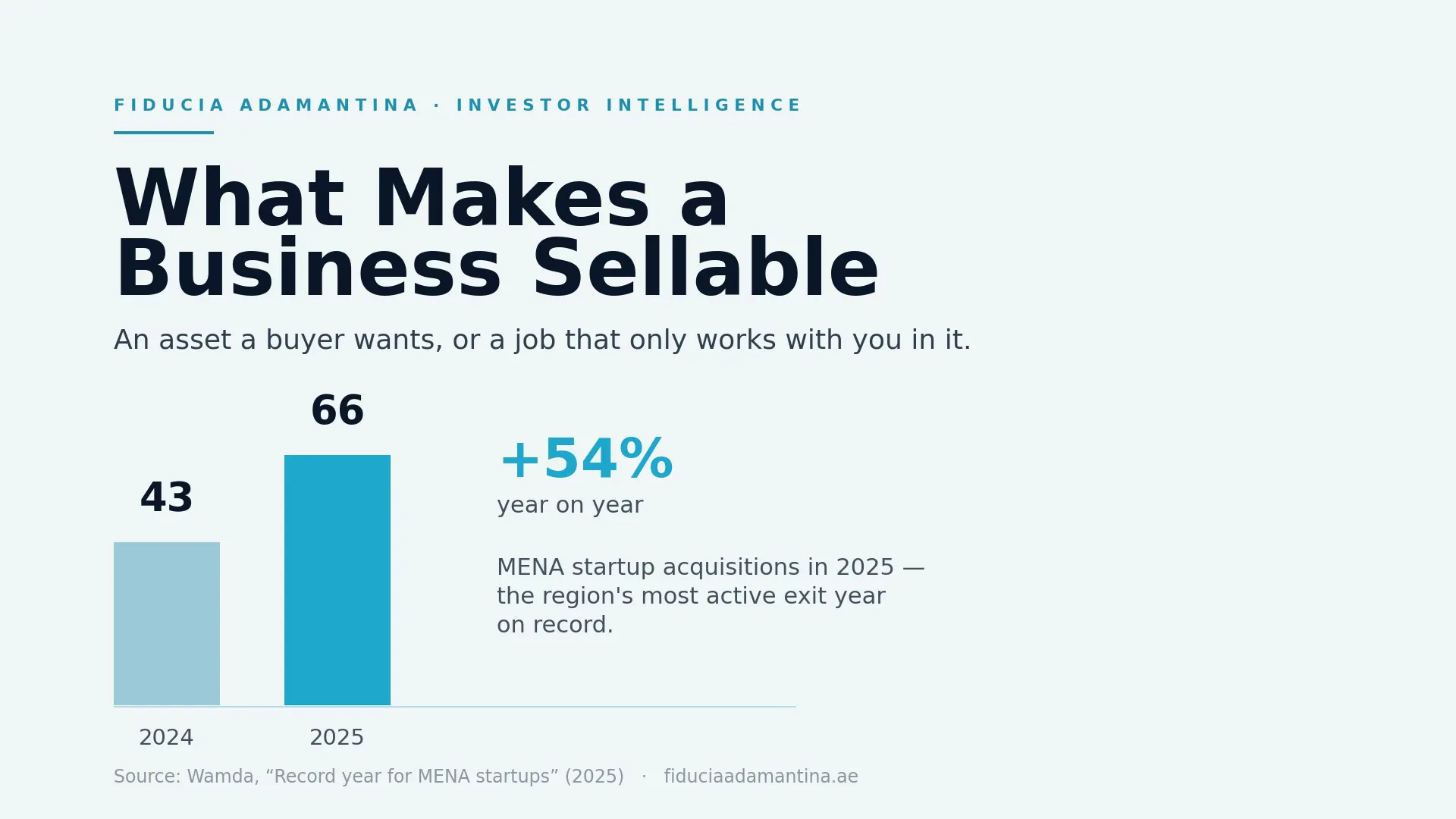

It matters more now because the exit market is real. Acquirers bought 66 MENA startups in 2025, up 54 percent on the year, according to Wamda, concentrated in fintech, SaaS, and e-commerce. More buyers are writing cheques. The founders who get paid well by them are the ones who built a sellable business years before the first conversation.

The question isn’t when you’ll sell, it’s whether anyone would buy

Sellability and timing are different problems, and founders confuse them constantly. When to sell your business is a question about markets, your own readiness to step away, and the cycle you are in. Whether the business is sellable at all is a question about what you have built. You can control the second one for years before the first one becomes urgent.

Here is the uncomfortable truth I put to founders early. A business that cannot run without you is not an asset. It is a job with your name on the lease. It might pay you well and feel like a company. But when a buyer looks at it, they do not see recurring cash flow they can own. They see a role they would have to fill with someone who is not you, doing work only you currently know how to do. That is not something people pay a premium for.

An asset a buyer wants, or a job that only works with you in it

The single test that separates the two is boring and brutal: could the business survive you being unreachable for two weeks? Not “would it be stressful,” but would decisions still get made, would customers still be served, would the important relationships hold?

For most founder-led companies the honest answer is no, and that is the first thing a buyer inspects. Not the growth rate, not the brand, but the degree to which the company is really just the founder wearing a corporate hat. Owner dependence is the risk buyers price most aggressively, because it is the risk that does not show up in the financials until after they have paid.

The fix is unglamorous and takes time, which is exactly why you start it three years out and not three months out. It means documenting how the business actually runs, so the knowledge lives in the company and not in your head. It means building a management layer that owns decisions you currently reserve for yourself. It means moving the key customer and supplier relationships off your personal mobile number and onto the company. None of it is fast. All of it compounds.

What buyers pay a premium for

Buyers do not pay for potential. They pay for risk they do not have to carry. Everything that reduces the risk of owning your company lifts what they will pay for it.

Within any sector’s valuation band, and value is always a range rather than a single number, which is why we anchor it to real comparables in our work on how SMEs are actually valued in a transaction, the same drivers move a company from the bottom of the band to the top. Growth is one. But the quieter three are revenue quality, customer concentration, and owner-independence.

Revenue quality means contracted, recurring income beats project or one-off income, because the buyer can underwrite it. Customer concentration means no single client should be so large that losing them breaks the business; as a rough working line, buyers I sit across from get uneasy when one customer is more than about a fifth of revenue. And owner-independence, again, is the one that quietly sets the ceiling. A business that scores well on all three sells near the top of its band. A business that is growing fast but depends entirely on the founder and one big client sells at a discount, no matter how good the top line looks.

What buyers quietly discount in diligence

The premium is only half the story. The other half is what gets stripped out once diligence starts, and this is where unprepared founders lose the most money.

A buyer’s diligence team is paid to find reasons to pay less. Unnormalised financials, related-party arrangements that were never documented, customer contracts that do not actually transfer on a sale, undocumented processes, a founder who is the only person who understands the numbers: each one becomes a line item in a price-chip conversation. The checklist a diligence team actually works from is public; the discounts they apply when your answers are weak are not, and they are large.

The mistake is treating all of this as something to clean up when a buyer appears. By then you are cleaning up under scrutiny, on the buyer’s timeline, with the price moving against you every week the process drags. Founders who prepare early are diligenced from a position of strength; founders who scramble are diligenced from a position of apology. This is the same discipline an exit and divestiture advisory process is built to impose, ideally long before you need it.

Exit readiness is the mirror of investor readiness

If any of this sounds familiar, it should. Everything that makes a business sellable to a buyer is nearly identical to what makes it fundable by an investor. Clean, normalised financials. A management team that is not just the founder. Revenue a stranger can underwrite. A data room that answers questions before they are asked. A defensible number backed by evidence, not hope.

Exit readiness and investor readiness test some of the same underlying evidence, but the fixed products do different jobs. The Investor Readiness Sprint builds the defined pitch materials and founder preparation; it does not remediate the company underneath them. The Exit Readiness Sprint applies a buyer lens and produces a 90-day plan, but it also stops before remediation. A stronger company may serve both audiences, but neither Sprint creates that strength in three weeks.

Your sellable business checklist starts three years early

If you want a working sellable business checklist, it is short, and none of it requires a buyer to be in the room. Can the business run for two weeks without you. Are the financials clean, normalised, and understood by someone who is not you. Is your revenue contracted and spread across enough customers. Do the key relationships and contracts belong to the company, not to you personally. Is there a management layer that owns real decisions. Could you hand a buyer a folder that answers the obvious questions without a scramble.

Every “no” on that list is both a discount at exit and, right now, a risk to the business you are running today. Fixing them makes the company more valuable to a buyer and more resilient in your hands in the meantime, which is the whole point of starting early. When you are ready to go deeper, our seven-gate exit-readiness framework walks through each gate a business clears before it goes to market.

Where to start before a buyer ever calls

You do not need to decide to sell to start building a business worth selling. You need an honest read on where you stand today.

The Exit Readiness Scorecard is a free self-assessment that scores your business across the dimensions a buyer actually inspects, from earnings quality and owner-independence to revenue durability, clean title, and process readiness, and it shows you where the gaps are while you still have years to close them. Run it now, not when an offer lands. The same readiness discipline sits behind our raise-side work, where the Investor Readiness Sprint does for a fundraise what exit preparation does for a sale.

If a buyer has already made contact, or you simply want a sharper read on what your business would be worth and where it is exposed, book a strategy session and we will walk through it with you before you are negotiating on someone else’s clock. The founders who sell well are almost never the ones who got lucky with timing. They are the ones who built an asset instead of a job, quietly, years before anyone made them an offer.