A broker told one founder his company was worth 8x. A friend in the same trade had just sold for 3x. Both numbers were defensible. The founder’s mistake was assuming one of them was a lie. They weren’t measuring the same thing, multiplying the same number, or pricing the same business, and until you can see why, every valuation you hear is noise.

This is the most common confusion I meet in valuation conversations, and it is not really about the multiple. It is about the number underneath the multiple. A founder hears “8x” and never asks “eight times what.” That single missing question is where most of the misunderstanding lives. So this is a walk through how small and mid-size companies are actually valued when they change hands: the earnings basis, the multiple range, the adjustments, and the gap between the headline figure and the money that reaches your account.

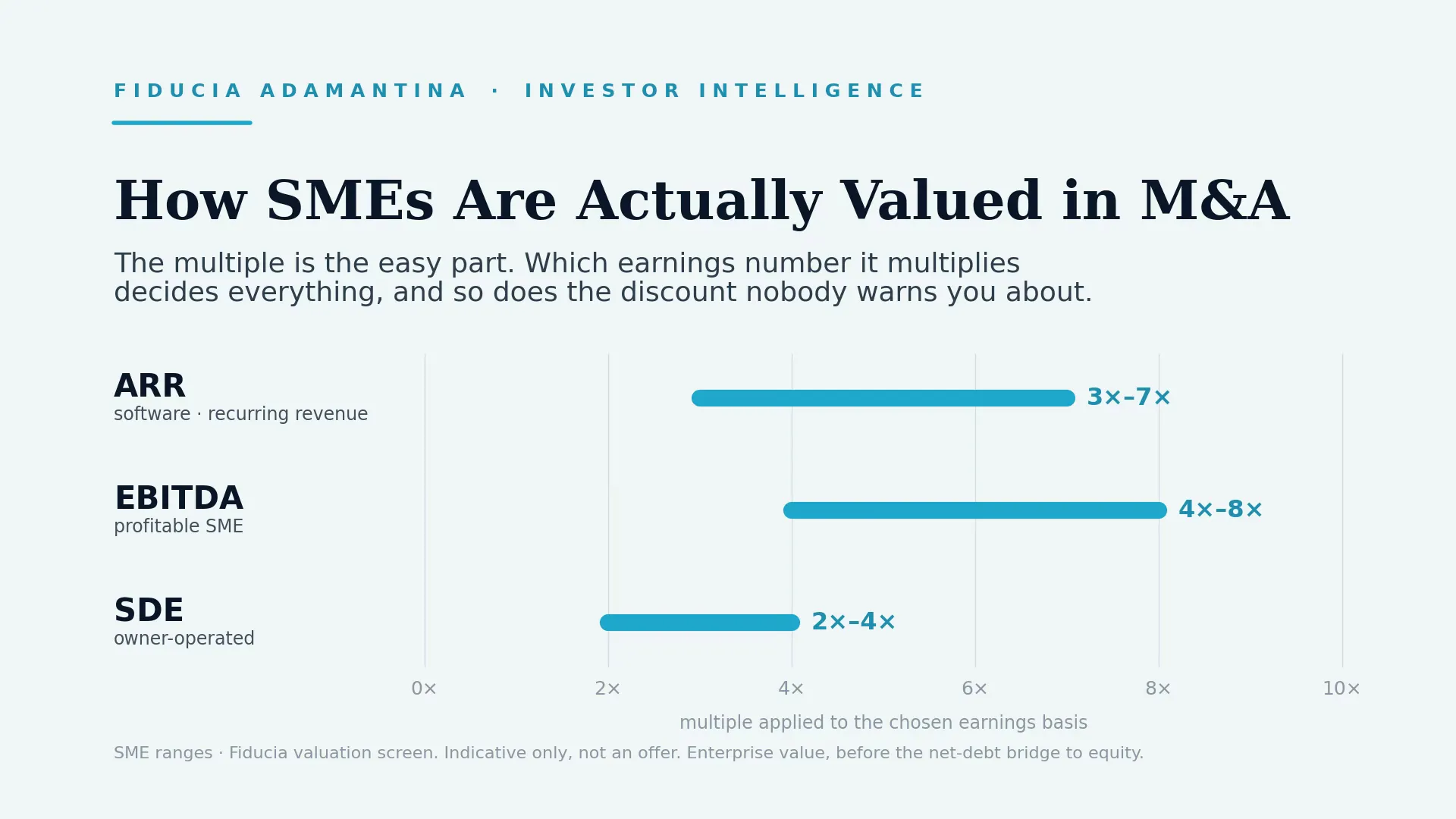

Step one is the number, not the multiple

Valuation has two moving parts: an earnings figure and a multiple applied to it. Founders fixate on the multiple. The earnings figure decides far more.

There are three bases a buyer might use, and which one applies depends on your size and how the business runs.

SDE, or seller’s discretionary earnings. Used for smaller, owner-operated businesses. It is profit with the owner added back in: your salary, your car, your discretionary costs, the perks that run through the company. SDE answers the buyer-operator’s question, “what will this business put in my pocket if I run it myself?”

EBITDA, earnings before interest, tax, depreciation and amortization. Used once a business is large enough to run without its owner, with a real management layer in place. EBITDA assumes the buyer pays a manager to do the owner’s job, so the owner’s compensation is a cost, not an add-back.

ARR, annual recurring revenue. Used for software businesses, where current profit understates the asset and recurring revenue is what a buyer underwrites.

The transition matters. Below roughly a million dollars of owner earnings, and especially when the company still depends on the owner, deals price on SDE. Above that, as a management team takes over the owner’s role, they price on EBITDA. Quote an EBITDA-style multiple against an SDE number, or the reverse, and you can misprice the business by a third without anyone lying to you. Your broker’s “8x” and your friend’s “3x” may simply have been multiplying different bases.

Normalized earnings: the number a buyer actually multiplies

Whatever the basis, no buyer multiplies the figure straight off your management accounts. They multiply a normalized number, and getting there is where founders most often lose value.

Normalization strips out what won’t continue under new ownership and adds back what was genuinely discretionary. Out come one-off items: the legal bill from a dispute that’s settled, the office move, the pandemic-era grant. Back come true owner add-backs: an above-market salary, a family member on payroll who doesn’t work in the business, the personal expenses that ran through the company. The goal is a clean, repeatable earnings figure that reflects what the business actually generates.

Two things go wrong here. Founders under-normalize, leaving discretionary costs in and handing the buyer a lower base than the business deserves. Or they over-normalize, claiming aggressive add-backs they can’t evidence, and a buyer’s diligence strips them out later, once the balance of power has shifted. The add-backs that survive are the ones with paper behind them. A valuation built on a number you can’t defend in a data room is a valuation that moves down once someone tests it.

Why your sector trades in a range, not at a point

Once the earnings figure is set, the multiple gets applied, and the multiple is a range, never a single number. Anyone who hands you one figure is selling certainty that doesn’t exist.

On the bands we screen against, a profitable small or mid-size company tends to change hands around 4x to 8x EBITDA, depending heavily on sector. Software is the outlier, priced on revenue, at roughly 3x to 7x ARR and stretching higher only for genuinely fast growth. Owner-operated businesses valued on SDE sit lower, commonly in the low single digits. Within any of those bands, where you land is set by company quality: size, growth, margin durability, customer concentration, how dependent the business is on you, and the mix of recurring versus one-off revenue. Recurring revenue is the single biggest lever. A service business with most of its revenue under contract trades meaningfully above the same business living job to job.

I won’t reprint a full sector table here, because a table is a lookup, not an answer, and the right basis and band for your business is exactly what a tool should pick for you. Our companion piece on EBITDA multiples by sector in the GCC lays out the bands and where private companies actually land relative to the headline numbers. The point to carry: a sector multiple tells you the neighbourhood, not the house.

The discount nobody warns founders about

Here is the trap that produces the “my friend got 8x, why am I offered 5x” conversation. The multiples founders read in industry reports and trade press describe large, listed, liquid companies: platforms with tens of millions in earnings, audited accounts, and a deep buyer pool. Your privately held business is smaller, harder to sell, more concentrated, and more dependent on a handful of people. Buyers price that difference.

The size-and-illiquidity discount against those headline comps typically runs around 15% to 35%, and wider still for the smallest companies. That is not a buyer being difficult. It is a methodological reality: the published multiple is a ceiling reference, not your sale price. The founders who feel ambushed are the ones who anchored on the ceiling and never knew the discount existed. The ones who hold their number understood the scale that actually applies to them before they took a meeting.

This is also why I’m wary of any “GCC multiple” or “Dubai market multiple” you might see quoted. Open-source transaction comps for private companies in this region don’t exist at that granularity. A regional multiple presented as fact is, more often than not, invented. The bands that hold up are global SME data adjusted for your specifics, not a number with a flag stuck on it.

Enterprise value is not what you keep

Suppose you’ve done it properly: right basis, normalized earnings, a defensible multiple. You now have an enterprise value. That is still not what you walk away with, and the gap surprises founders at the worst possible moment, the closing table.

Enterprise value is the value of the business operations. What reaches your account is equity value, and getting from one to the other means crossing the net-debt bridge: subtract debt, add back surplus cash, then adjust for a working-capital target the buyer expects the business to be delivered with. Two businesses with identical enterprise values can pay out very differently depending on what sits on the balance sheet. A founder who quotes the multiple-derived figure as “what I’m getting” has skipped the step that decides their actual proceeds.

If you want to see these mechanics on your own numbers rather than in the abstract, our valuation calculator walks the full chain. It picks the earnings basis for your sector, applies a realistic SME range instead of a public-market headline, and runs the enterprise-to-equity bridge, returning an indicative range rather than a false-precision point. It is the fastest honest read on where your business sits before you trust anyone’s verbal number.

The number is only as good as the model under it

Every step above rests on one thing: the quality of your numbers. A buyer who can’t trust your reporting discounts the whole business, because if the financials are loose, what else is? The single highest-return preparation a founder can do is make the earnings figure clean, evidenced, and impossible to argue down.

That is harder than it sounds, and the same errors recur: add-backs with no support, revenue recognized early, owner costs tangled into operating costs, a model that can’t tie back to the bank. I pulled the ones that cost founders the most into a short read, the Financial Model Mistakes Guide. If a sale or a raise is anywhere on your horizon, fix these before anyone runs diligence on you. A clean model doesn’t just defend your multiple, it moves you up inside the band, because reporting quality is one of the factors buyers price.

It’s the same discipline whichever direction you’re heading. On the raise side, the work of making a company legible to an investor, clean numbers, a defensible story, a data room that holds, is exactly what our Investor Readiness Sprint builds. On the sell side, the goal is the mirror image: a number a buyer can’t pull apart. The underlying job is identical, which is why valuation work is never wasted regardless of which exit you take.

Run your own number, then pressure-test it

So the next time someone hands you a multiple, run the checklist before you believe it. Which earnings basis, SDE, EBITDA, or ARR? Is the number normalized, and can every add-back be evidenced? Is the multiple a range with a reason for where you sit in it, or a single figure sold as certainty? And does it stop at enterprise value, or has someone walked it down to what you’d actually keep?

Valuation sits early in the M&A process, and it sets the anchor for everything that follows: the asking price, the negotiation, what survives diligence. Getting it wrong at the start is expensive to correct later, when a buyer is holding a signed letter of intent and a deadline. Getting it right early is the cheapest edge you have.

A defensible number is also the first thing that separates a credible process from a hopeful one. Whether your next step is a raise, where the Investor Readiness Sprint turns your numbers into materials an investor will back, or a sale, the work is the same: know your real number, and be able to prove it.

If a sale is on your horizon, the most useful thing you can do now is learn what a buyer would conclude. Book a strategy session and we’ll walk your business through the same valuation lens an acquirer’s team will use: the right basis, a defensible range, the bridge to your real proceeds, except earlier and on your side of the table. The founders who negotiate from strength are the ones who knew their number, and could defend it, before anyone put one on the table. Our overview of M&A advisory in Dubai covers what that support involves.