A founder considering fundraising support should be able to answer three questions before signing: what exactly will I receive, when does the clock start, and what will still be my responsibility afterward?

The Investor Readiness Sprint answers those questions with a fixed scope. It costs AED 25,000 and takes 2–3 weeks from complete intake. It builds the defined investor-facing materials and prepares the founder to present them. It does not make the underlying company inherently investable or automatically ready for Due Diligence.

That distinction matters. A coherent deck cannot repair weak traction. A financial model cannot create missing evidence. A cap-table scenario cannot execute legal changes. The Sprint improves what can be built and presented from the available facts, while identifying the issues that still require management, legal, accounting, tax, or other specialist work.

Before Day 1: complete intake

The delivery clock does not start merely because a kickoff call has been booked.

Before Day 1, we need the current pitch deck if one exists, historical financial information, management forecast assumptions, the current cap table, founding documents, the raise target, intended use of funds, and the founder’s availability for prompt factual feedback.

If a required source input is missing, we cannot present it as fact. Client-caused delay pauses the delivery clock; it does not expand the scope.

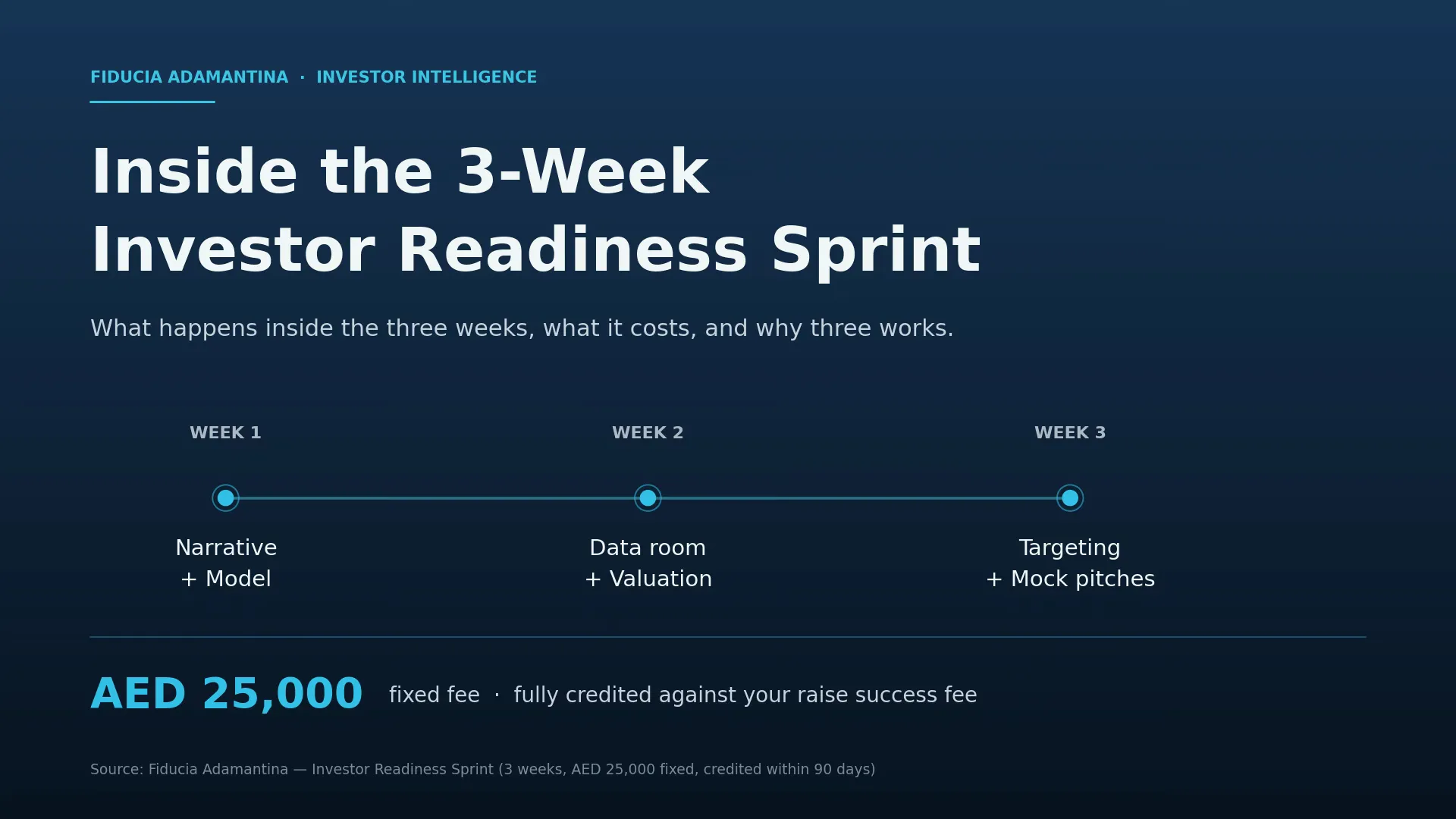

Week 1: audit the inputs and lock the story

Week 1 starts with the company as it actually exists: its product, market, traction, business model, economics, raise, and intended milestones.

We audit the current deck, financial information, cap table, and structure. We then agree the investor narrative and map the assumptions that must sit behind it. The purpose is not to invent certainty. It is to separate supported facts, management assumptions, and open questions before they are embedded in the materials.

Week 2: build the deck, model, and cap-table scenario

The core build has three connected parts:

- A 10–15 slide pitch deck covering the agreed investor story, market, business model, traction, economics, raise, use of funds, and milestones.

- One bottom-up operating model based on management-supplied actuals and assumptions, with unit economics where applicable, base/downside/upside sensitivities, use of funds, runway, and milestone logic.

- The current ownership position and one post-raise or conversion cap-table scenario, with material red flags and open questions identified.

Fiducia does not audit or independently verify management inputs inside the Sprint. The cap-table work is modelling and commercial review, not legal advice, document execution, ESOP implementation, vesting changes, or confirmation that the structure is clean.

One consolidated factual revision is included. Additional companies, raises, operating models, narratives, or revision rounds require separate written scope.

Week 3: rehearse, finalise, and hand over

Week 3 turns the working materials into an owned delivery pack.

The founder receives the final editable deck and model, the cap-table output, pitch and objection notes, the pre-meeting checklist, and the investor-research framework. We run one live rehearsal so the founder can explain the assumptions, defend the use of funds, and recognise questions that require further evidence rather than an improvised answer.

The result is a pitch-materials package ready for investor conversations. That is not the same as saying the company is fully investor-ready.

What is outside the AED 25,000 Sprint

The fixed fee does not include:

- Investor introductions, a named investor list, placement, solicitation, or Fiducia-led outreach

- Data-room build or population, Due Diligence management, investor Q&A management, negotiation, or closing support

- Legal, tax, regulatory, audit, bookkeeping, accounting-restatement, valuation, or market-validation work

- Corporate restructuring, cap-table cleanup, ESOP implementation, vesting changes, or document execution

- Independent verification of forecasts, market size, traction, contracts, or financial information

- Any guarantee of investor interest, a term sheet, valuation, timing, or funding

If the company needs those things, the answer is not to stretch the Sprint until its price and deadline become fictional. The answer is a separate prerequisite or engagement.

Where Sprint + Go-to-Market fits

The AED 40,000 Sprint + Go-to-Market tier includes the same materials build plus 30–45 days of support while the founder runs their own outreach. It adds outreach scripts, an investor-tracking pipeline, a weekly operating rhythm, meeting preparation, weekly office hours, and one commercial term-sheet read-through if a term sheet arrives during the engagement.

It still does not include investor introductions, placement, Fiducia-led outreach, legal term-sheet advice, or full raise execution. Those remain separate mandate work.

Price, payment, and optional credit

The Investor Readiness Sprint is AED 25,000, normally paid 50% at kickoff and 50% on delivery. It is independently buyable; no raise mandate or success fee is required.

If the client later appoints Fiducia on the raise within 90 days, paid Sprint fees are eligible for credit up to AED 25,000 against the raise success fee under the mandate terms. Whether we take a raise mandate at all is solely our decision, on our capacity and our read of the company. Continuation is optional. The Sprint’s value is the work delivered, not the possibility of a later mandate.

Start with the Investor Readiness Scorecard if you need a directional view first. If the fixed scope fits the gap, review the full Investor Readiness Sprint page before booking.