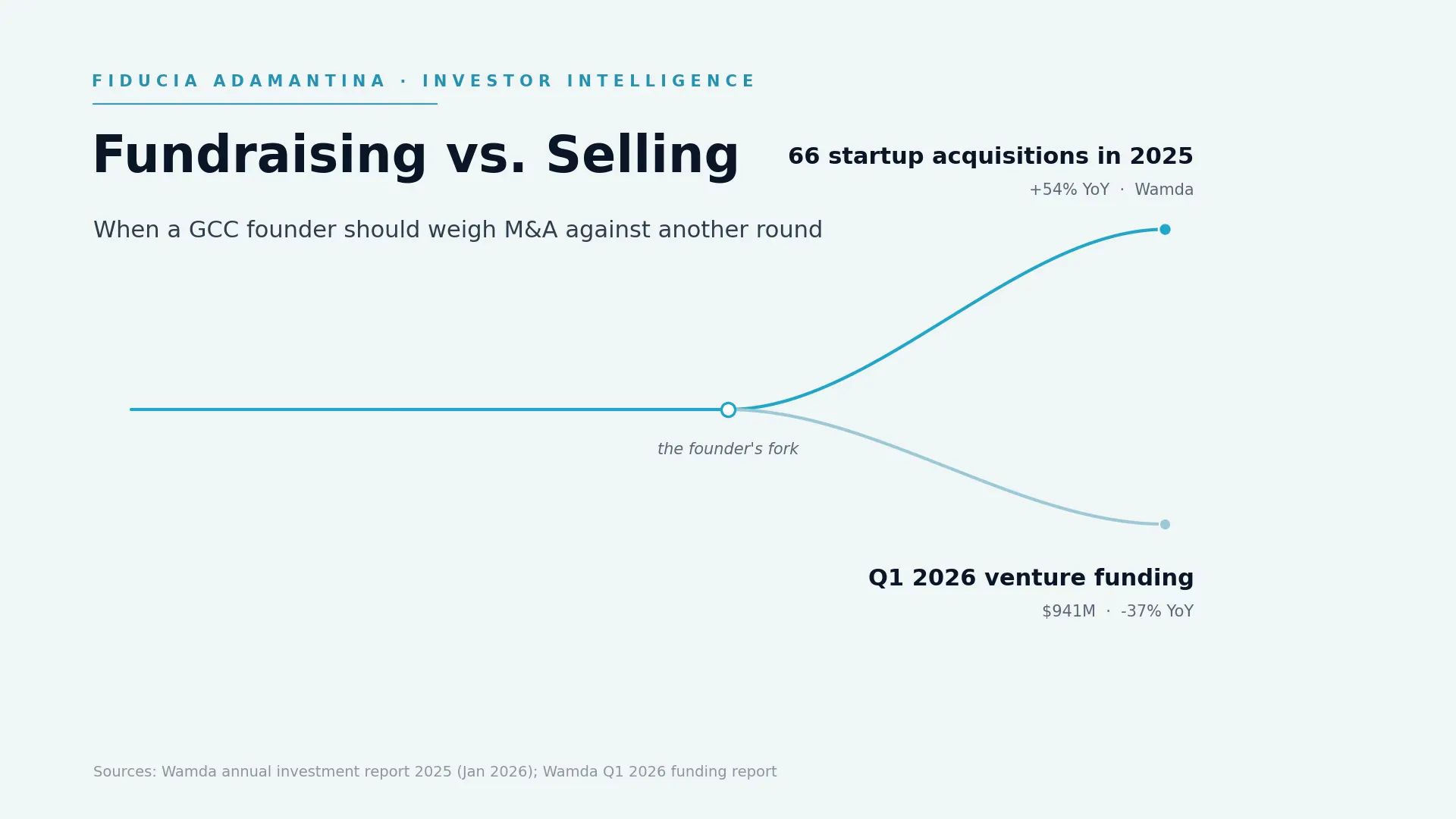

Acquirers bought 66 MENA startups in 2025, up 54 percent on the year, the region’s busiest exit year on record, according to Wamda. Then first-quarter 2026 venture funding came in at $941 million, down 37 percent year on year. More buyers at the table, slower cheques from the funds. If you are a founder sitting between rounds, the market has quietly changed the shape of your decision.

The version of that decision I hear in our practice rarely arrives as “should I sell my startup.” It arrives as a confession: “I’m exhausted from fundraising. Someone mentioned I could sell instead. But isn’t that giving up?” That last question is the expensive one, because it turns a strategy decision into an identity test. Founders who treat a sale as failure tend to consider it two years too late, after the negotiating position is gone.

What follows is a framework for taking the identity out of it.

Fatigue is information, not weakness

Founders who ask me about selling almost never open with the word “sell.” They open with the raise. The last round took the better part of a year. The next one means another two quarters of full CEO attention spent on process instead of product.

Take that seriously as a signal. A raise is not a transaction you delegate; it consumes the founder. If the honest reaction to starting another one is dread rather than appetite, that tells you something real about the next three years of your life, because the next round is never the last demand the venture path makes of you.

And then set it aside, because fatigue alone is a bad reason to sell. Buyers price distress quickly, and a process entered from exhaustion reads as exhaustion in every management meeting. The work is separating “I am tired of fundraising” from “this business is worth more inside someone else’s portfolio than it is standalone.” The first is a state. The second is a thesis. Only the second belongs in front of a buyer. Once that second reason is real, how to sell a business in Dubai walks the process itself.

What the 2025–2026 market is actually telling you

Three numbers from the same Wamda dataset are worth holding together.

First, the headline: 647 MENA startups raised a combined $7.5 billion in 2025, up 225 percent on the year. Second, the caveat inside it: $4 billion of that was debt, and stripping debt from both years leaves equity investment up a more sober 77 percent. Third, the exit line: 66 acquisitions, up 54 percent, concentrated in fintech, SaaS, and e-commerce and centred on the UAE, Egypt, and Saudi Arabia. Which of those acquirers you end up in front of matters — selling to a competitor versus PE versus a search fund shapes both price and what happens to you after close.

Wamda’s own reading of 2025 was a region entering “scale and selective consolidation.” I agree, and the first quarter of 2026 sharpened the point: funding cooled 37 percent while the consolidation logic kept running. Acquirers do not stop buying when venture sentiment softens. Often they buy more, because targets get cheaper and competition from new funding rounds thins out.

For a founder, the practical meaning is this: the sell side of the table is more real in the GCC than it was two years ago, and the raise side is slower than the 2025 headlines suggest. Neither fact decides your case. Both should inform it.

Five questions that decide between a raise and a sale

In our practice I run founders through five questions. None of them mentions feelings, which is precisely the point.

1. Does your next milestone need capital, or a parent? If what blocks growth is money to spend on a motion you already run well, that argues for raising. If what blocks growth is something an acquirer already owns (distribution, licences, a balance sheet, enterprise relationships you would spend years building), the strategic value of being inside their portfolio may exceed anything you can build standalone with another round.

2. What does the maths say, dilution against the waterfall? A credible offer today competes against the next round’s dilution plus the exit you would need in three years to beat it. Most founders have never run that comparison properly. The section below covers it.

3. Are you selling into strength or out of fatigue? The strongest exits I have seen were negotiated with twelve months of runway and a growth story still compounding. The weakest were forced conversations with one quarter of cash left. If you may want to sell within two years, the time to create buyer relationships is while you still do not need them. I cover the timing side of this in more depth in when to sell your business.

4. Where is your sector on the consolidation clock? The 2025 exit record was not evenly spread; it clustered in fintech, SaaS, and e-commerce. Consolidation waves reward early sellers and punish late ones, because each acquisition removes a buyer from the pool. If two of your direct competitors have been acquired in eighteen months, the question is no longer abstract.

5. Who actually controls the decision? Your cap table votes. Liquidation preferences, board composition, drag-along rights, and the fund-cycle position of your largest investor can all make a sale easier or harder than you assume. Knowing this before a buyer calls is the difference between leading the conversation and being led through it.

What an M&A process asks of a founder-led company

Founders consistently underestimate how much an acquisition process demands of the company rather than the deal team. Diligence on a founder-led business goes deeper than most Series A diligence: revenue quality, customer concentration, contract assignability, IP chain of title, and, hardest of all, founder dependence. A business that cannot run without you is, to a buyer, a salary negotiation wearing a company’s clothes.

I have written a full walk-through of how the merger and acquisition process actually runs, stage by stage, and a companion piece on the questions to ask a potential acquirer before you are deep in their process. The short version: the preparation that survives buyer diligence is substantially the same preparation that survives investor diligence. Clean financials, a defensible valuation story, a data room that answers questions before they are asked. The two paths diverge at the destination, not at the start.

The GCC dynamic: your buyer may not be a fund

Here the region genuinely differs from the markets most M&A content is written for. In the GCC, the active acquirer set extends well beyond financial sponsors: listed corporates, sovereign-linked groups, and family conglomerates buy companies to import capability, not to flip them. The landmark regional example remains Uber’s $3.1 billion acquisition of Careem in 2019, a strategic purchase of market position and local capability, and still the benchmark every regional exit conversation starts from.

Family groups change the texture of a sale. They hold for decades, they care about management continuity, and they frequently want the founder to stay and build inside the group. For a founder whose alternative is another dilutive round followed by a forced exit on a fund’s timetable, that profile can be a better owner, and the price negotiation runs on strategic value rather than venture comparables. It also means your buyer list in this region should be built deliberately. The obvious acquirers are rarely the complete set.

The maths conversation: dilution against the waterfall

Strip the emotion out and the raise-versus-sell question becomes one comparison: what a sale returns to you today against what your stake survives to be worth after another round and a later exit.

The sale side of that comparison should not be a guess. Run the valuation calculator first: it returns an indicative enterprise-value range anchored to your sector’s multiple band, with the net-debt bridge to equity, so “what a sale returns today” enters the maths as a range rather than a hope.

Run it honestly and the inputs get uncomfortable. A new round takes dilution off the top. The new investor’s liquidation preference stacks on top of the existing ones, and in a modest later exit the preference stack eats from your share first, not theirs. Most founder models I review price only the headline valuation and overestimate the founder’s own outcome in the mid-range scenario, which is the scenario that usually happens.

This is exactly the modelling most founder financial models cannot do, because they were built to sell a growth story rather than to compare outcomes. I have collected the failure patterns in our Financial Model Mistakes Guide, and the waterfall blindness above is among the most common and the most costly. If you take one piece of homework from this article, build that comparison before you talk to anyone, buyer or investor.

When the answer is still to raise

Most founders who work through the five questions land on raising, and they should. If the business is compounding standalone, the category is still expanding rather than consolidating, and the milestone ahead needs fuel rather than a parent, then a sale today sells the steep part of your own growth curve to someone else at a discount.

What changes after this exercise is the quality of the decision. A founder who has run the waterfall maths, stress-tested founder dependence, and looked honestly at the buyer landscape enters investor meetings with an answer to the question every serious investor silently asks: what happens if the next round does not come? If the decision is to raise, the Investor Readiness Sprint can build the defined deck, model, cap-table scenario, and founder preparation. It does not build the data room or repair company-level gaps; those remain separate work whichever door you choose.

Deciding in practice

If this article found you mid-decision, do two things in order.

First, get an objective read on where you stand. Run the waterfall comparison with the Financial Model Mistakes Guide open beside your model, then take the Investor Readiness Scorecard, a free self-assessment that surfaces the gaps a raise process or a buyer’s diligence will find. Together they replace a 2 a.m. feeling with a structured picture.

Then map the path that matches your lean. Our Get deal-ready hub lays out both tracks. If it is towards raising, the Investor Readiness Sprint delivers the fixed pitch-materials package in 2–3 weeks from complete intake, with an optional 90-day raise-mandate credit. If it is towards selling, or you genuinely cannot tell, book a strategy session and we will work the five questions against your actual numbers. The wrong choice here is not raising or selling. It is deciding by default.