Blog

Read, Learn, and Grow

Explore insights, trends, and expert perspectives on fundraising, private equity, M&A, and business consulting from your trusted investment consultant in Dubai.

How Much Should You Actually Raise? Round-Sizing Logic Investors Respect

"Why this number?" is a test. The median gap between rounds is 696 days. Size the round backwards from the milestone, not from a figure that felt right.

27 Jul 2026Read Post →

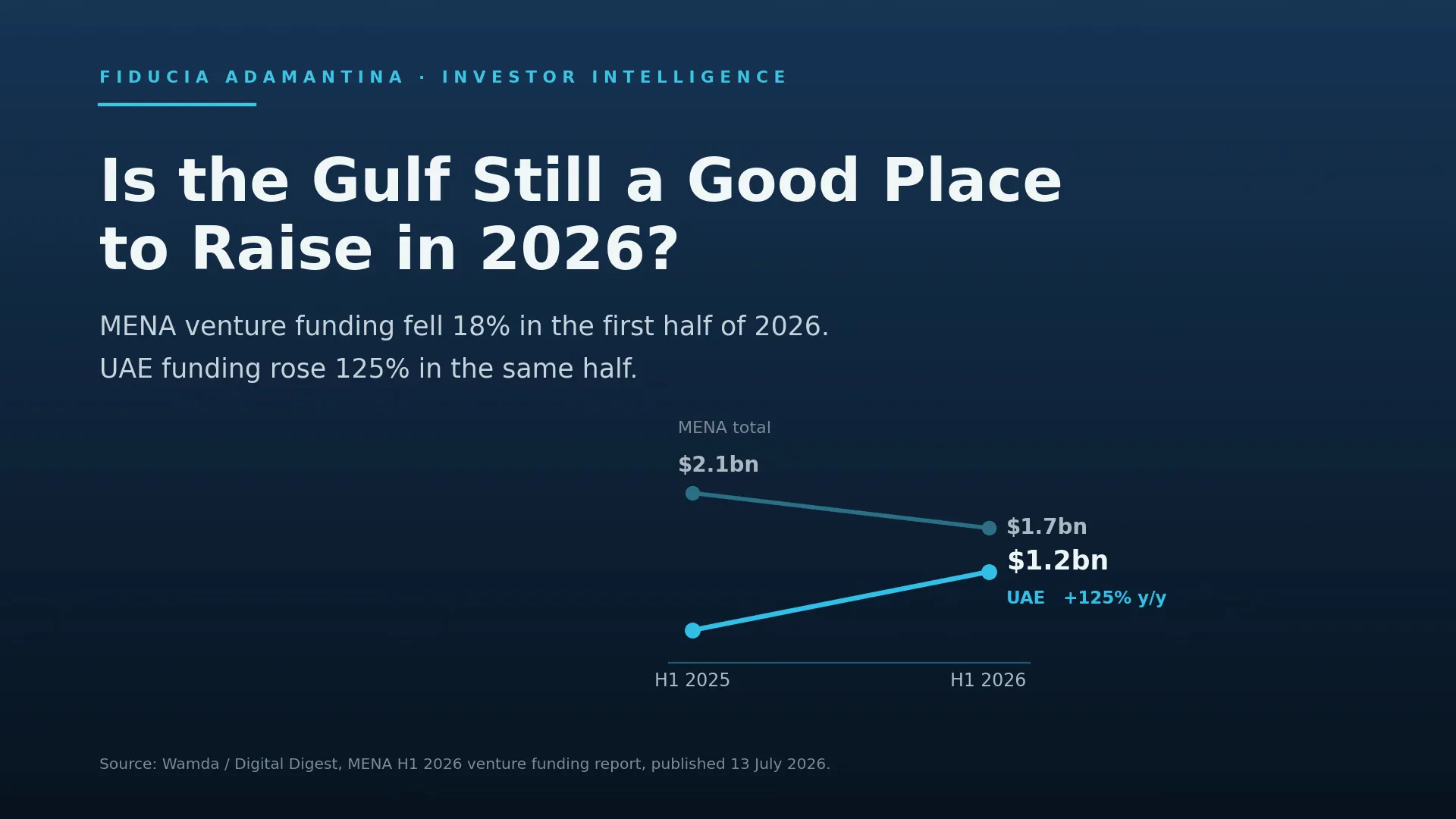

Is the Gulf Still a Good Place to Raise in 2026? An Honest Read of the Data

MENA funding fell in H1 2026 while UAE funding rose 125%. An honest read of the data on who the Gulf actually works for — and who it doesn't.

20 Jul 2026Read Post →

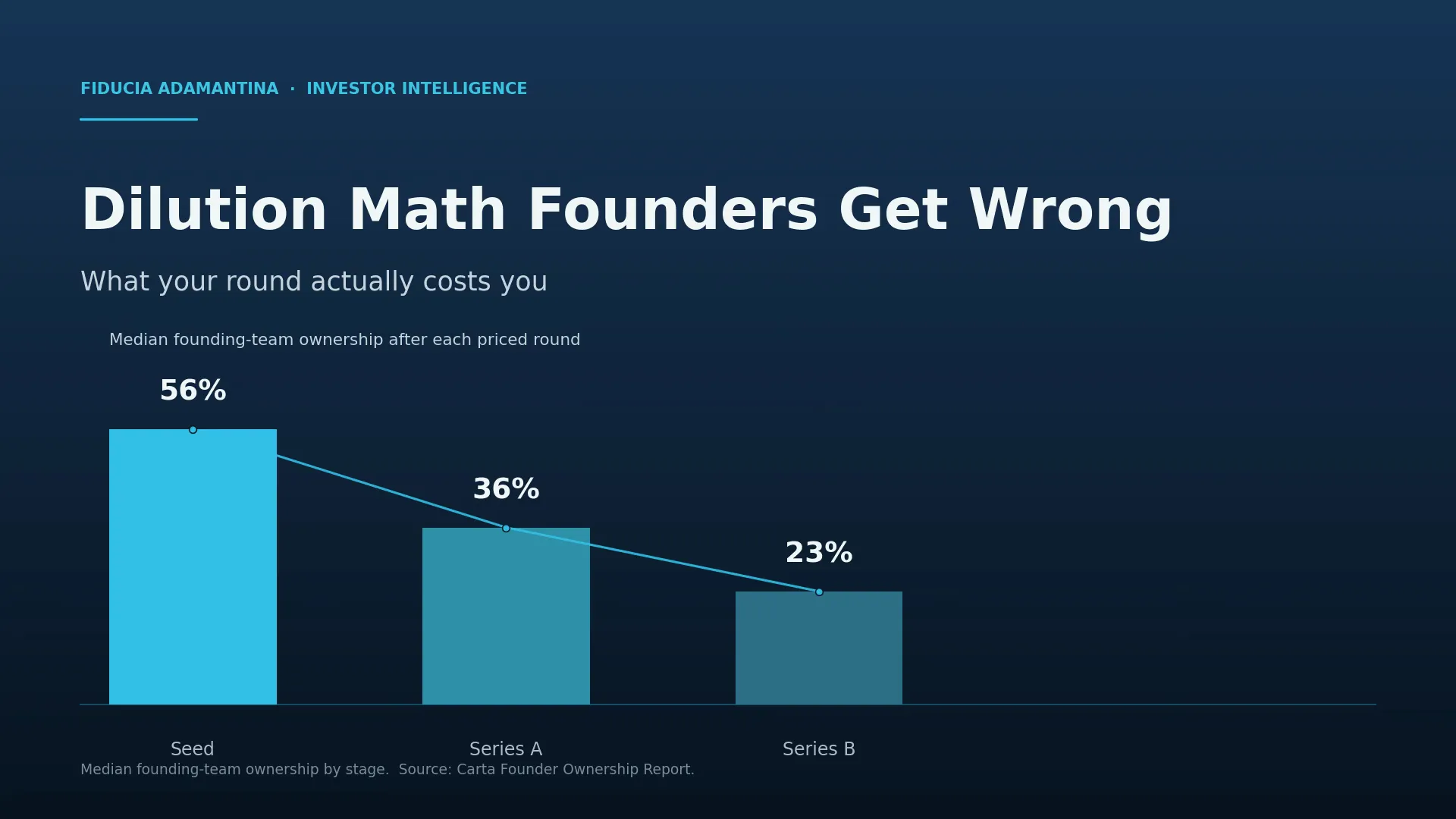

Dilution Math Founders Get Wrong: What Your Round Actually Costs You

You own 62% on paper. After the option-pool top-up, two SAFEs converting, and a priced round, you own 37%. The dilution math, worked end to end.

16 Jul 2026Read Post →

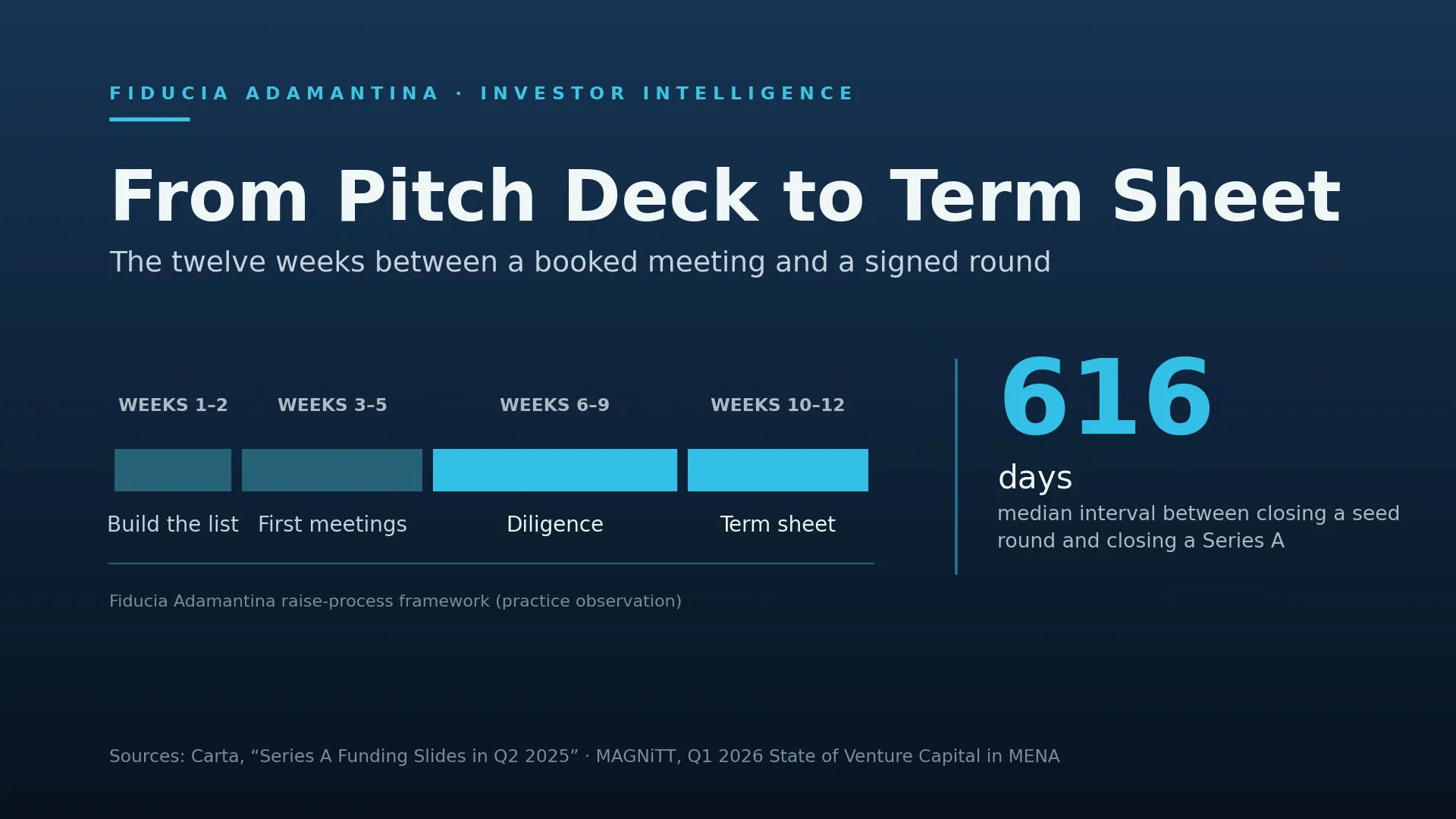

From Pitch Deck to Term Sheet: The Founder's Roadmap to Closing a Round

The real timeline from first investor meeting to signed term sheet: what happens in each phase, why rounds stall, and what to build before you start.

13 Jul 2026Read Post →

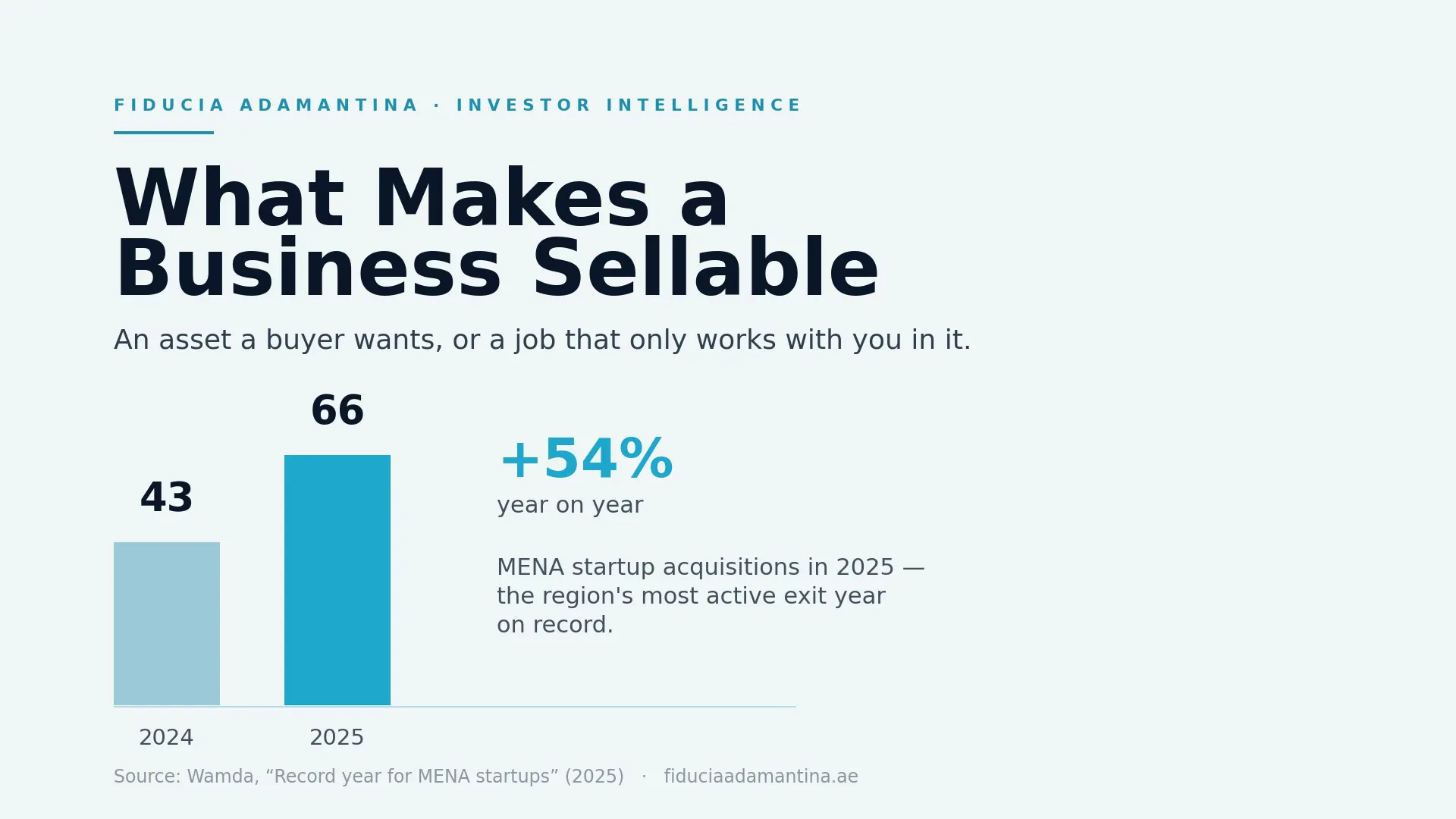

What Makes a Business Sellable: An Asset, Not a Job

You might sell in a few years. Are you building an asset a buyer pays a premium for, or a job that depends on you? What makes a business sellable.

9 Jul 2026Read Post →

Strategic Acquirer or Financial Investor: Which Fits Your Business?

A corporate group wants to invest and hints at buying you. A fund offers a growth round. How strategic and financial capital differ for GCC founders.

6 Jul 2026Read Post →

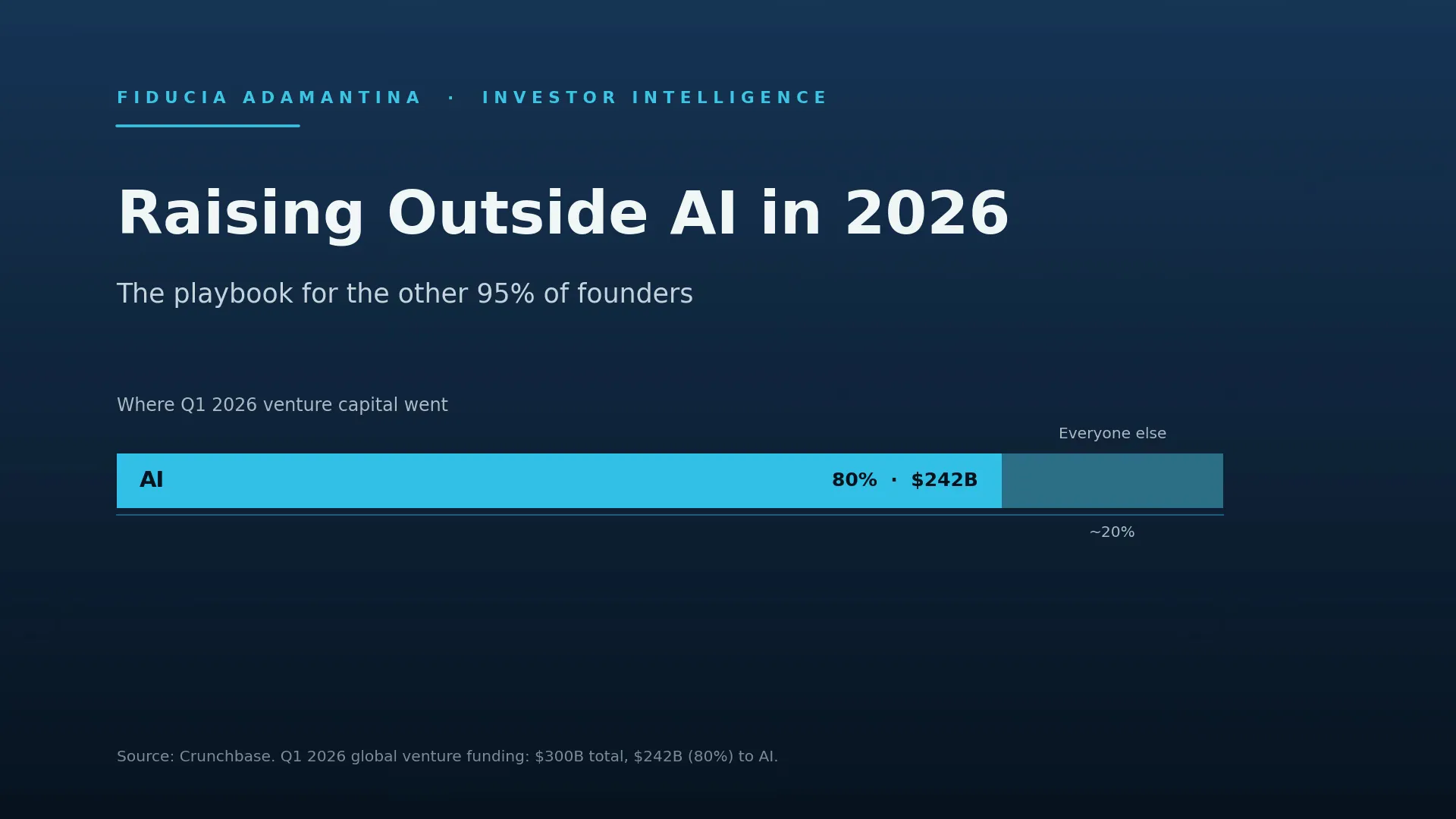

Raising Outside AI in 2026: The Playbook for the Other 95% of Founders

Q1 2026 VC hit a record $300B and 80% went to AI. The honest playbook for the other founders raising in a market that isn't chasing them.

2 Jul 2026Read Post →

The Hidden Costs of Going to Market Without Advisory Support

DIY fundraising looks free until you count the lost months, the burned introductions, and the valuation you give away. The real math for founders.

29 Jun 2026Read Post →

How to Sell a Business in Dubai: A Founder's Step-by-Step Guide

Most Dubai business sales disappoint for the same reason — the owner went to market unprepared, to one buyer, with no process. Here is how to do it properly.

29 Jun 2026Read Post →

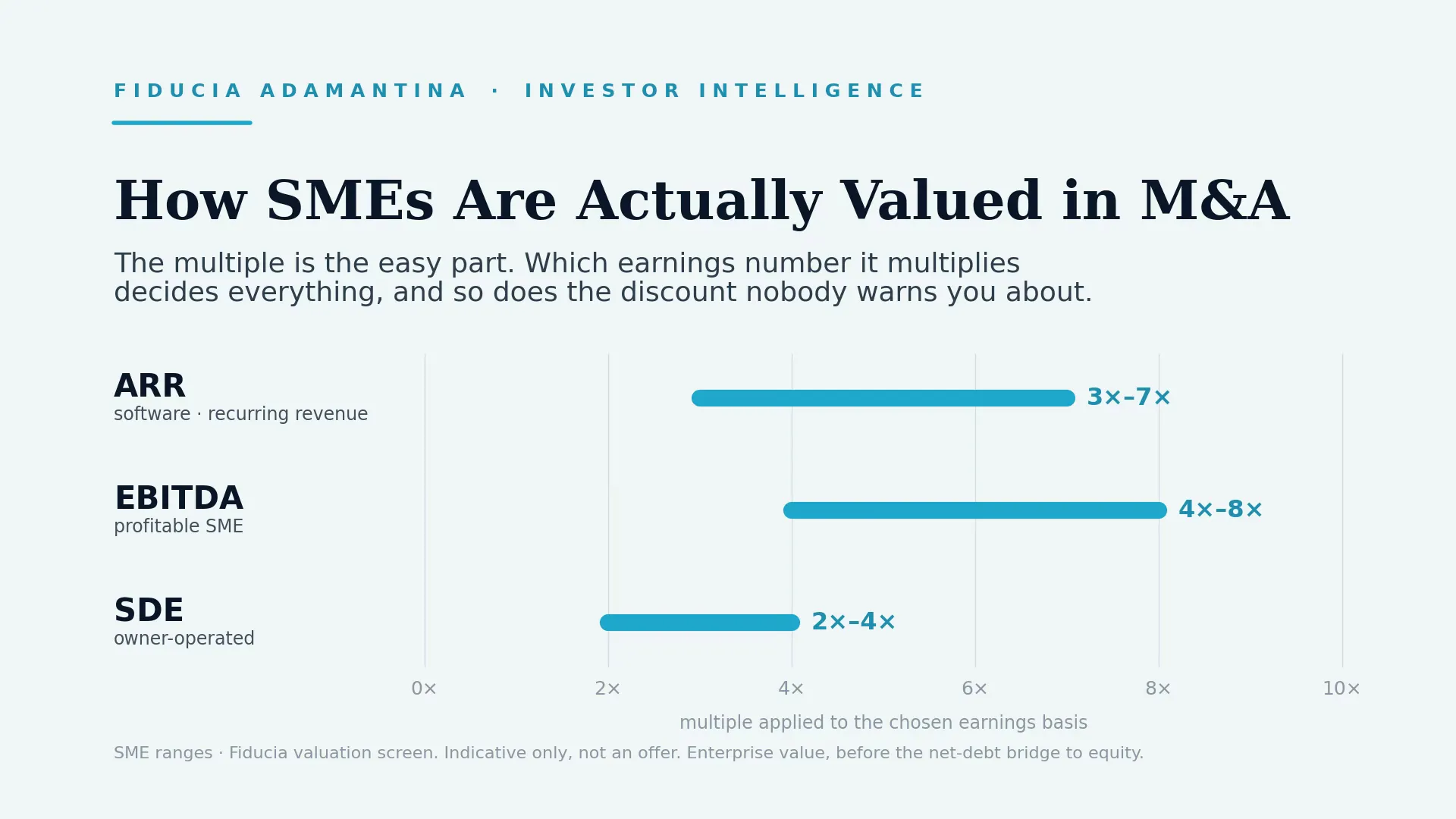

How Small and Mid-Size Companies Are Actually Valued in M&A: EV/EBITDA, SDE, and Your Real Number

A broker says 8x, a friend sold for 3x. How small and mid-size companies are really valued in M&A: EV/EBITDA, SDE, and the number you actually keep.

25 Jun 2026Read Post →

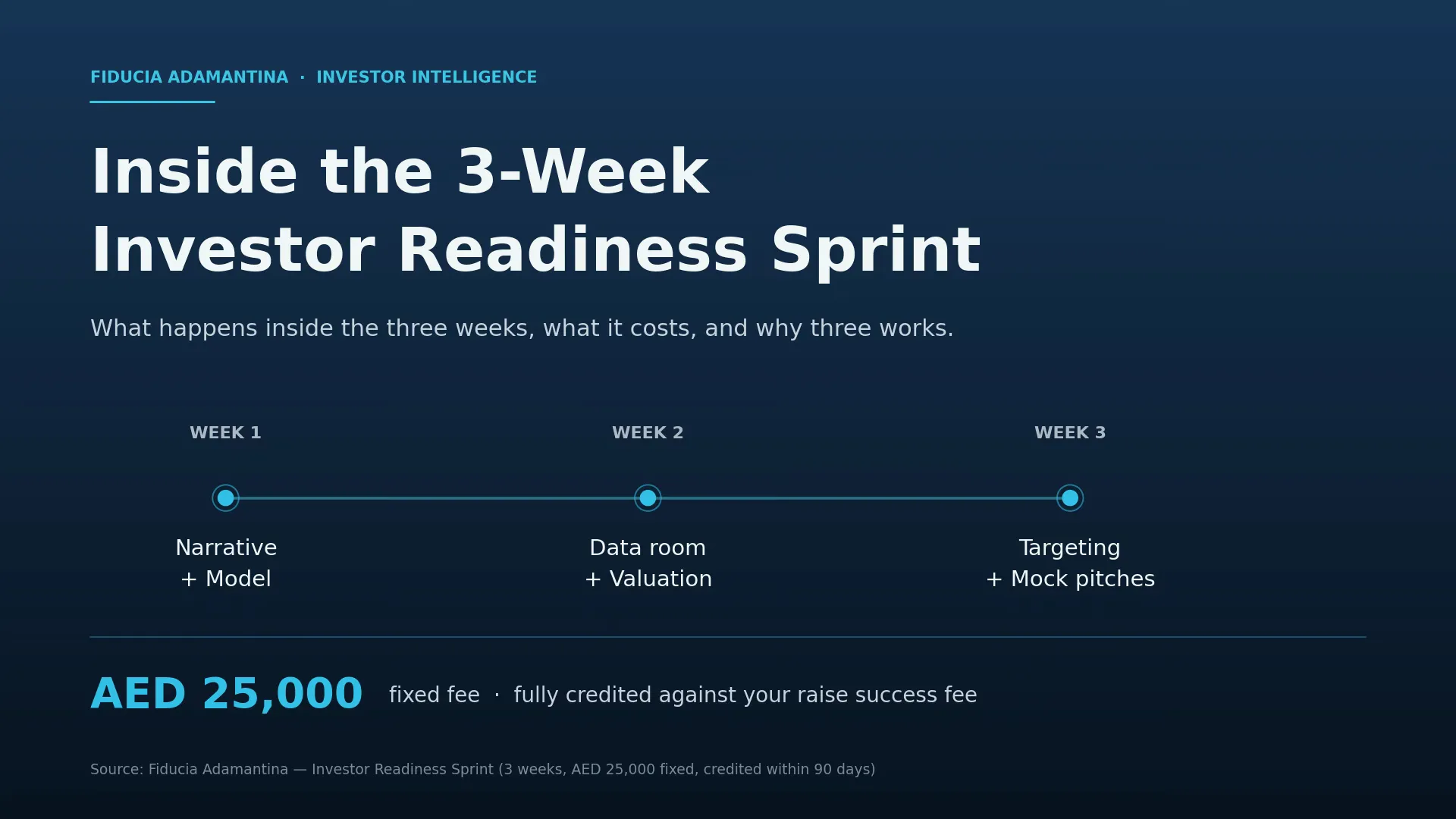

Inside Our 3-Week Investor Readiness Sprint: What Happens and What It Does Not Do

What the AED 25,000 Investor Readiness Sprint delivers in 2–3 weeks, what the client must provide, and which company-readiness gaps remain outside scope.

22 Jun 2026Read Post →

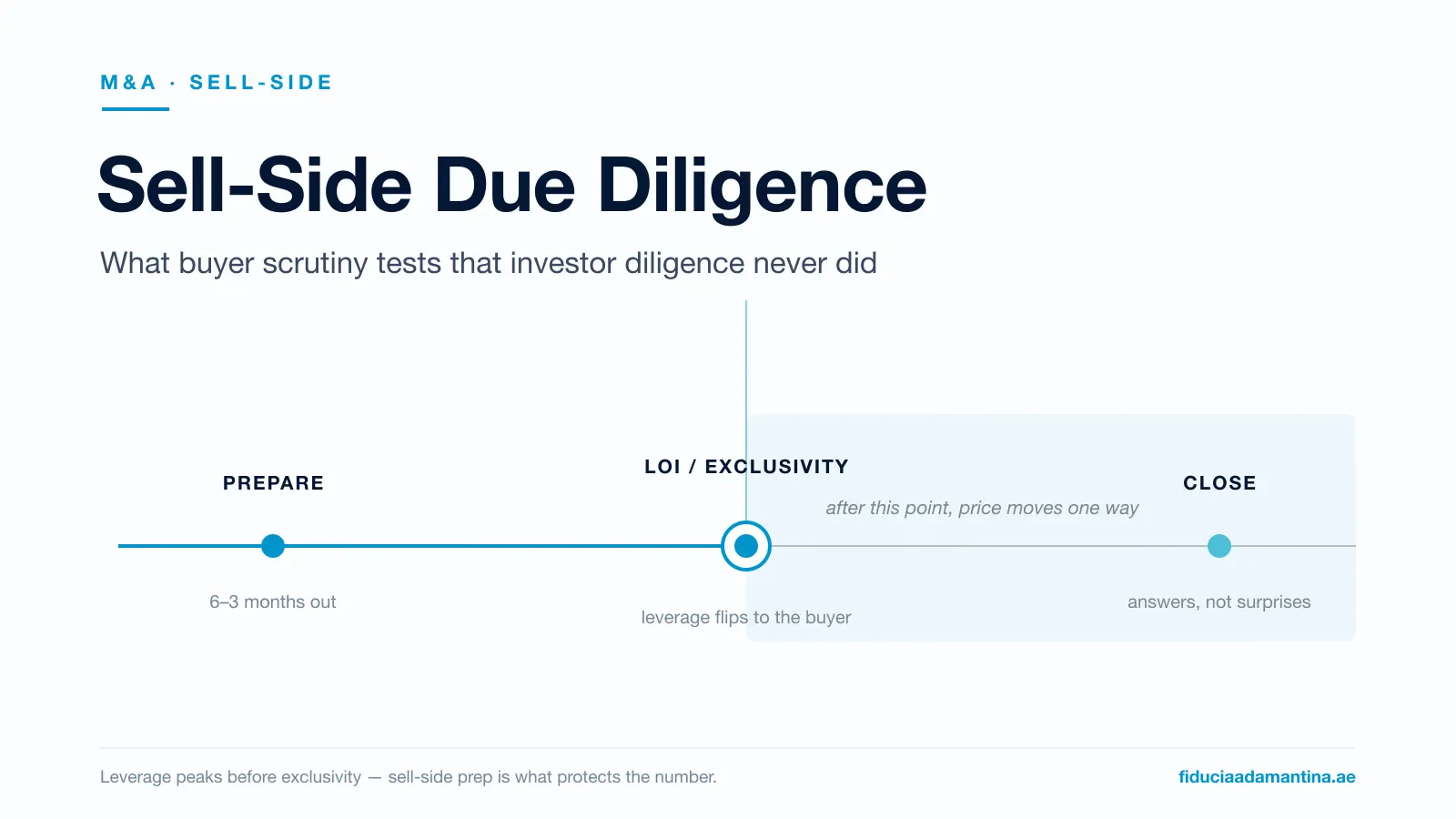

Sell-Side Due Diligence: How to Prepare Your Company for Buyer Scrutiny

A buyer sent a 200-line diligence request and half is unfamiliar. What buyer scrutiny tests that investor diligence never did, and how to prepare early.

18 Jun 2026Read Post →

The Number That Survives Diligence: a QoE & EBITDA add-back benchmark

The adjusted EBITDA a seller presents and the EBITDA that survives diligence are two different numbers — and the multiple applies to the second one. Which add-backs buyers challenge, why audited accounts aren't enough, and the GCC family-business twist.

15 Jun 2026Read Post →

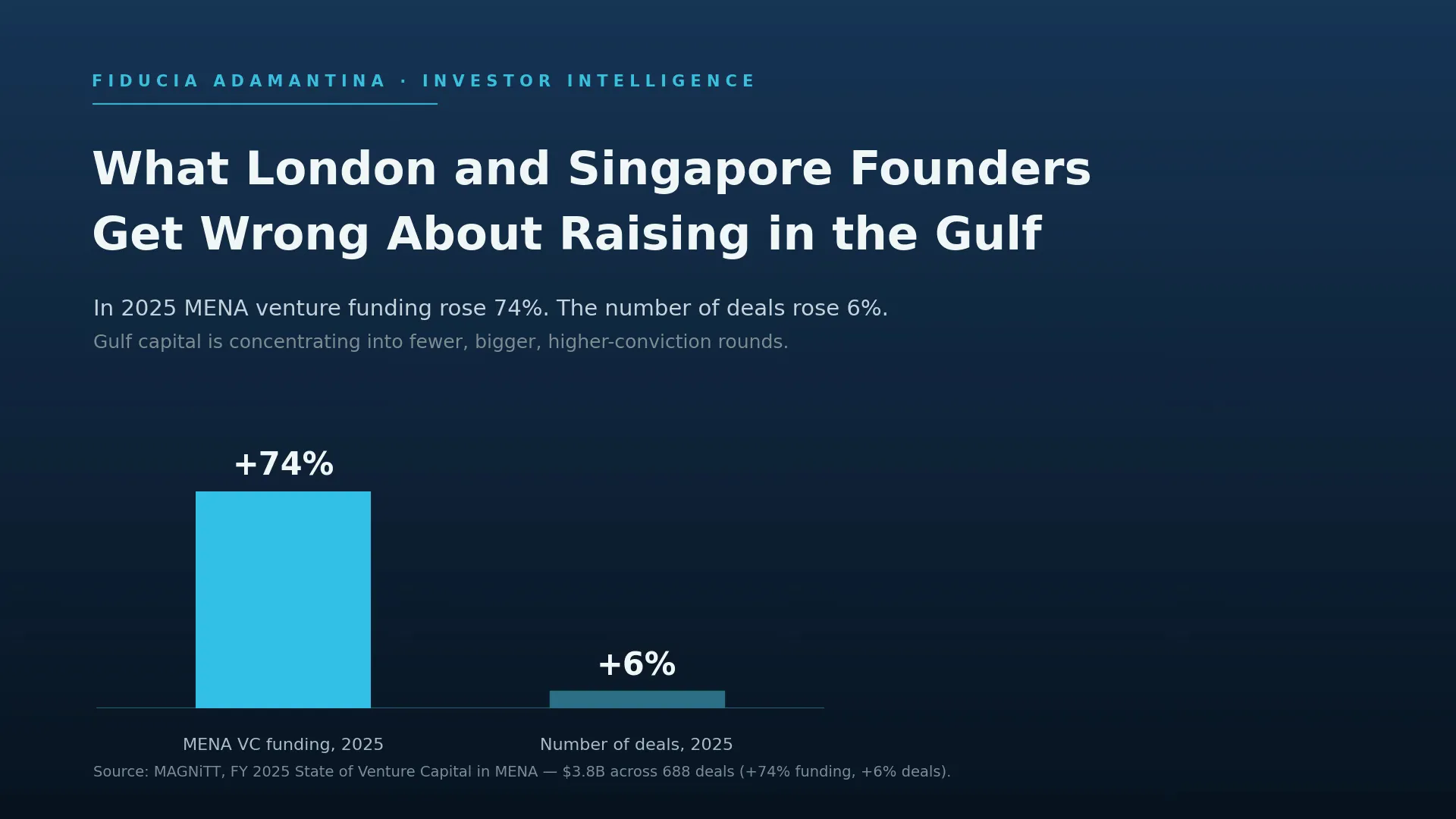

What London and Singapore Founders Get Wrong About Raising in the Gulf

Your deck raised a round in London but drew blank stares in Dubai. Five reasons Gulf investors pass on international founders, and how to fix each.

15 Jun 2026Read Post →

GCC M&A Deal-Structure Benchmark: How Sellers Actually Get Paid

The headline price isn't what you keep. How much of a sale is cash vs earnout vs escrow, how little earnouts actually pay, and the one insurance lever that cuts a seller's at-risk money from 10% to near zero.

14 Jun 2026Read Post →

The GCC M&A & Founder Exit Report 2026: Multiples, Deal Activity, and What Actually Closes

A founder-facing read of the GCC deal market: 2025's record M&A year, the 2026 cooling, what private businesses sell for, and the generational-transfer wave driving exits across the Gulf.

13 Jun 2026Read Post →

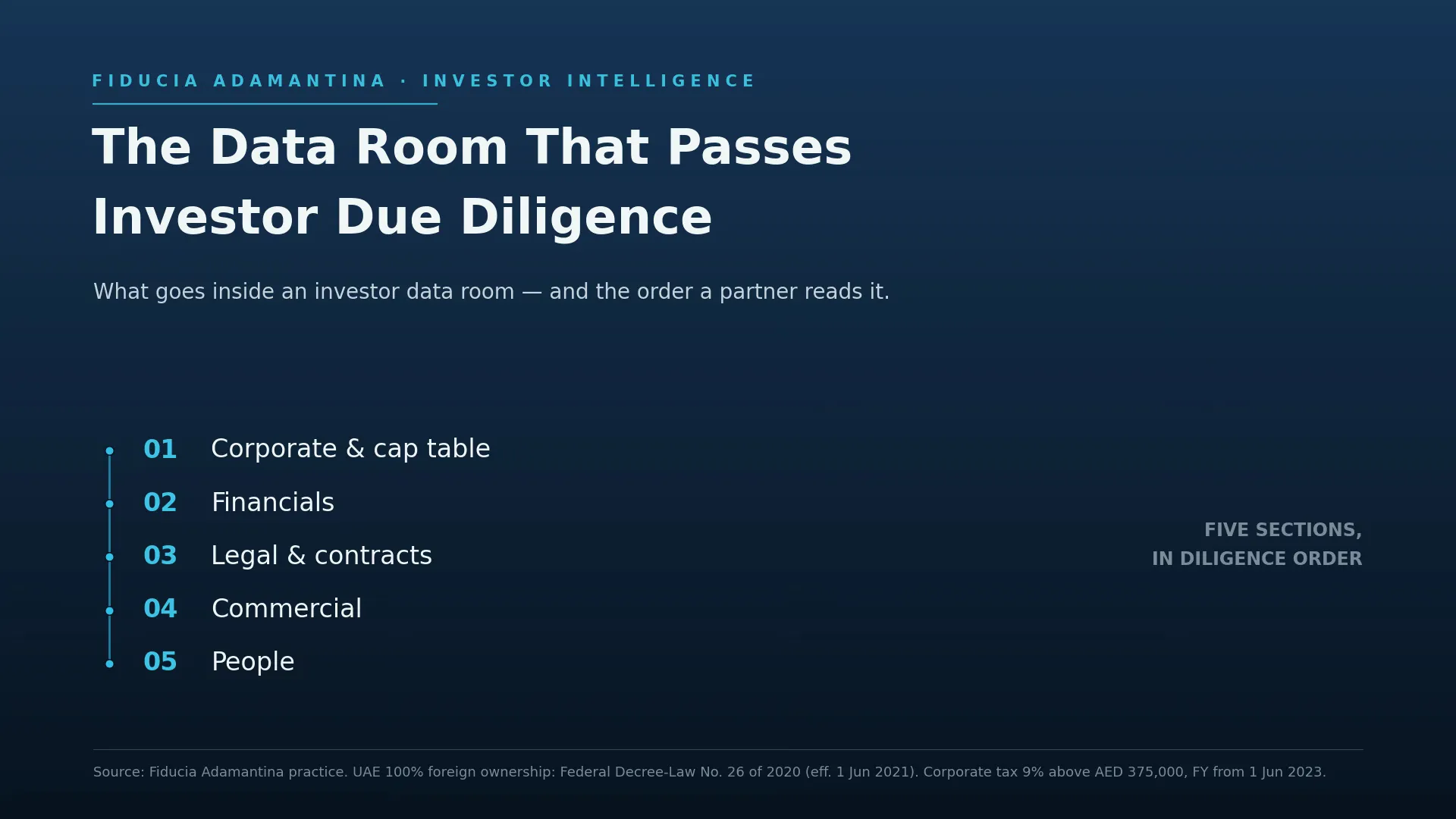

How to Prepare a Data Room That Passes Investor Due Diligence — First Time

An investor asked for your data room and you froze. Exactly what GCC investors expect inside, and how to build one that speeds the raise.

11 Jun 2026Read Post →

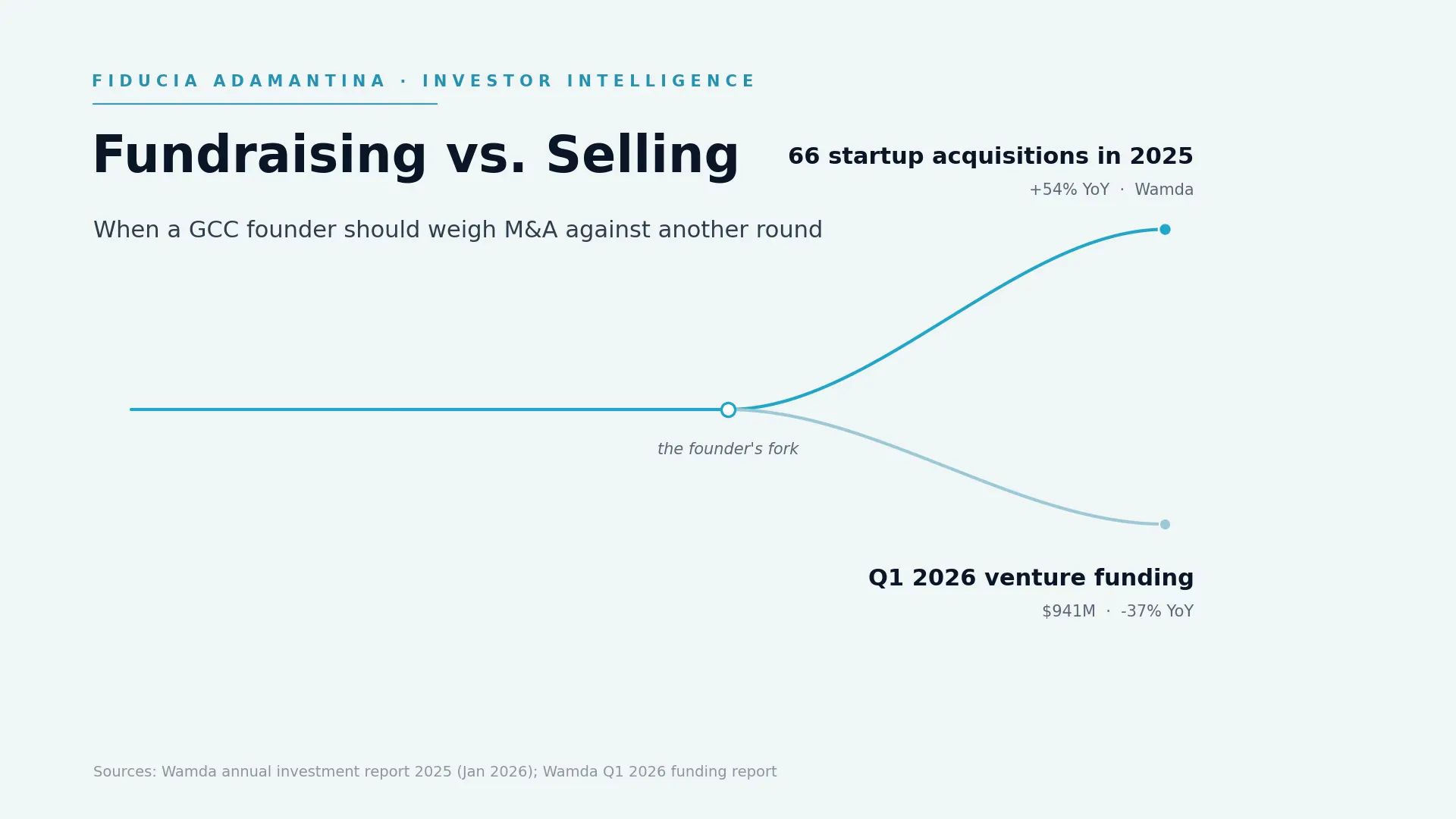

Fundraising vs. Selling: When a GCC Founder Should Consider M&A

MENA logged 66 startup acquisitions in 2025 while Q1 2026 funding fell 37%. A working framework for founders weighing another round against a sale.

8 Jun 2026Read Post →

EBITDA Multiples by Sector in the GCC: What Your Business Will Actually Sell For (2026)

The multiples you've seen quoted are for listed giants, not private companies. The realistic EV/EBITDA bands a GCC business actually sells for, by sector — and the adjustments that move you inside the range.

7 Jun 2026Read Post →

MENA Startup Funding Benchmark 2026: round sizes, stages & what actually closed

What MENA startups actually raised: the record 2025 totals, why two different headline numbers both circulate, the UAE-vs-Saudi split, why there's no clean 'average round size', and the regional valuation-data gap founders keep getting burned by.

6 Jun 2026Read Post →

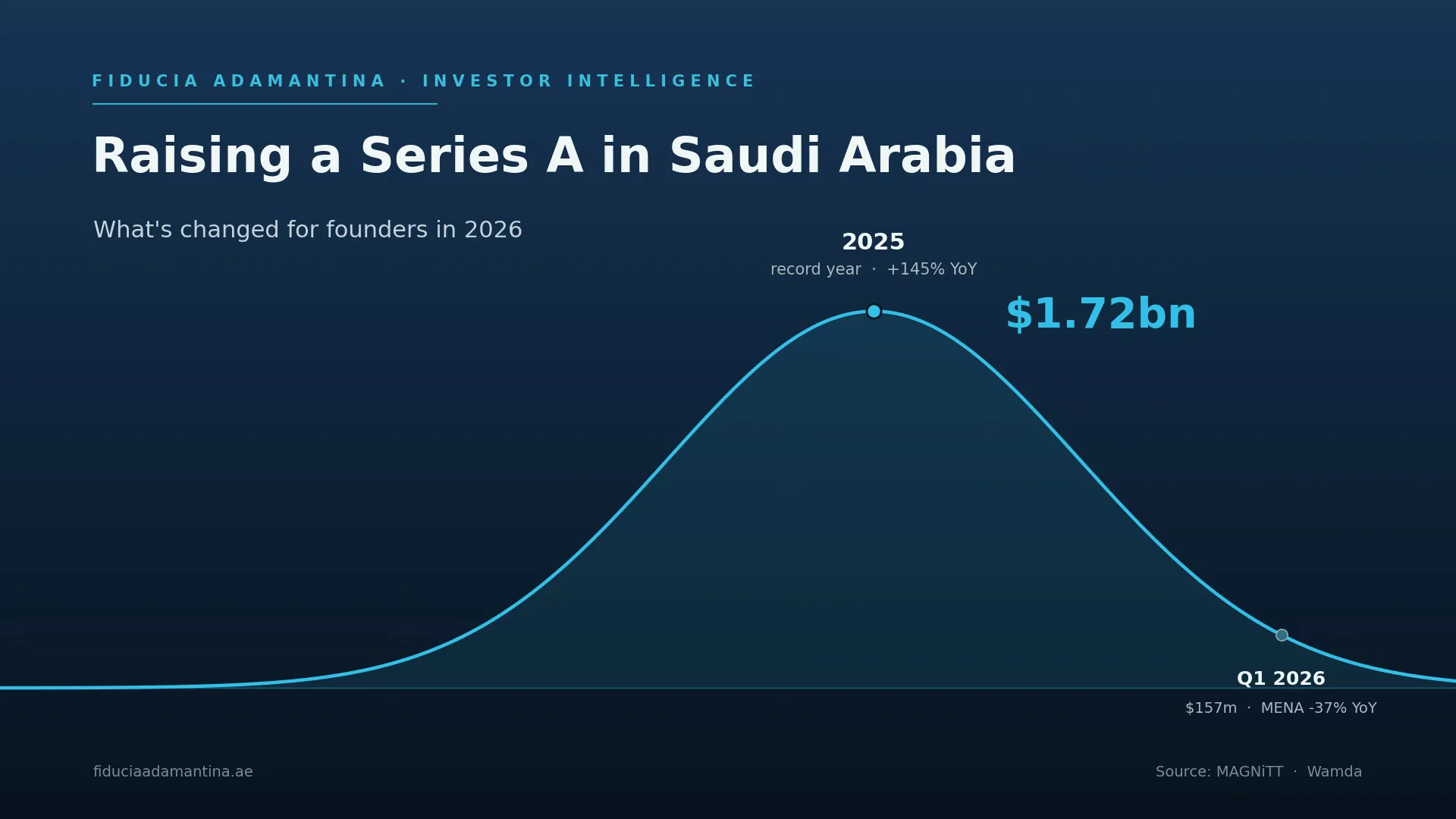

Raising a Series A in Saudi Arabia: What's Changed for Founders in 2026

Saudi led MENA venture funding in 2025, then Q1 2026 cooled. A current read on the players, the RHQ shift, and raising a Series A in the Kingdom now.

4 Jun 2026Read Post →

How to Build a Financial Model That MENA Investors Actually Trust

What MENA investors actually scrutinise in a fundraising model, and the cost-base, FX, and unit-economic gaps that lose the room.

1 Jun 2026Read Post →

GCC Founder Dilution Benchmark: How Much of Your Company You Actually Give Up (2026)

There is no published dilution benchmark for Gulf founders — so most over-dilute by default. The real numbers (founder vs investor ownership by stage), the ESOP trap, and the term-sheet economics that protect you.

31 May 2026Read Post →

The Exit Readiness Framework: The 7 Gates a GCC Business Clears Before It Goes to Market

Buyers pay a premium for businesses that are ready to be bought — and discount the rest in diligence. The seven gates a GCC company should clear before it goes to market, from the seller's side.

30 May 2026Read Post →

Is Your Startup Investor-Ready? Take This 5-Minute Self-Assessment

Pitching before you are investor ready burns introductions that cannot be re-run. A five-minute self-assessment that tells you whether to take the meeting — or close the gaps first.

25 May 2026Read Post →

What Acquirers Actually Pay: a GCC buy-side pricing & control-premium benchmark

How acquisition prices are really set: the control premium over standalone value, why strategic buyers pay more than private equity, the size discount that prices small companies below big ones, and who the GCC buyer pool actually is.

24 May 2026Read Post →

Venture Debt vs Equity for Gulf Founders: The Non-Dilutive Question to Ask Before Your Next Round

GCC venture debt grew ~8x in four years — yet most Gulf founders still default to an equity round. When non-dilutive capital fits, what it costs, who actually lends in the region, and the trap to avoid.

23 May 2026Read Post →

Raising in the UAE as a Foreign Founder: What to Know First

An incoming founder's guide to raising in the UAE — DIFC vs ADGM, the 100% foreign ownership rules that still bite, investor access, and 90-day sequencing.

18 May 2026Read Post →

Who's Buying Gulf Companies: a GCC cross-border & foreign-buyer M&A benchmark

Most of the money in Gulf M&A crosses a border. The domestic-vs-inbound-vs-outbound split, who the foreign buyers actually are, the sovereign-fund outbound engine, and how the UAE's 100% foreign-ownership reform widened the buyer pool.

17 May 2026Read Post →

How to Raise From Family Offices in the GCC: A Founder's Playbook

Family offices are the Gulf's deepest and least-understood capital pool — and founders keep pitching them like VCs. The GCC family-office map, why they now back founders, and how to actually get a cheque.

16 May 2026Read Post →

Why Most Founders Fail Their First Investor Meeting — And How to Fix It

A diagnostic walk through the five preparation gaps that decide whether a first investor meeting becomes a second.

11 May 2026Read Post →

What GCC Investors Actually Look For (Beyond Your Revenue Numbers)

Capital is still flowing into the Gulf — it's just flowing toward founders who have done the work investors don't put on the slide deck.

4 May 2026Read Post →

How to Value Your Startup Before Fundraising in the Middle East

A practical guide for founders preparing to raise in the Middle East, covering the valuation frameworks GCC investors actually anchor to.

27 Apr 2026Read Post →

Investor Readiness Framework: 5 Pillars That Decide Whether You Get the Round

The five pillars GCC and international investors actually judge you on before a raise — narrative, model, data room, valuation, and investor fit.

21 Apr 2026Read Post →

7 Pitch Deck Mistakes That Turn Off GCC Investors (And What to Do Instead)

GCC investors close decks in 30 seconds when they spot these 7 mistakes. Learn what turns off Gulf investors and how to fix your pitch.

13 Apr 2026Read Post →

How to Raise Funding in the UAE: A Step-by-Step Guide for Founders

A GCC-specific guide to raising startup funding in the UAE — from angels and VCs to government-backed funds, across Dubai, Abu Dhabi, and beyond.

6 Apr 2026Read Post →

Life After the Sale: Earn-Outs, Transition Periods & Staying On

The day after you sign, you are still in the building — but the chair is no longer yours. What a good advisor tells a founder about transition, earn-outs and the identity shift, before the ink dries.

20 Jan 2026Read Post →What Not to Tell a Buyer in Early Conversations

A coffee, a friendly question, a number you can't take back. What founders over-share in early buyer conversations — and what to say instead.

16 Dec 2025Read Post →

Buy-and-Build in the GCC: How Add-On Acquisitions Create Value

One clinic is worth 5x earnings. Five clinics run as one are worth 8x. Buy-and-build, and how add-on acquisitions create value in fragmented GCC sectors.

18 Nov 2025Read Post →What Actually Happens in the First 30 Days of a Sell-Side Mandate

A week-by-week walk through the first month of a sell-side mandate — where most of the value is built before a single buyer is contacted.

21 Oct 2025Read Post →

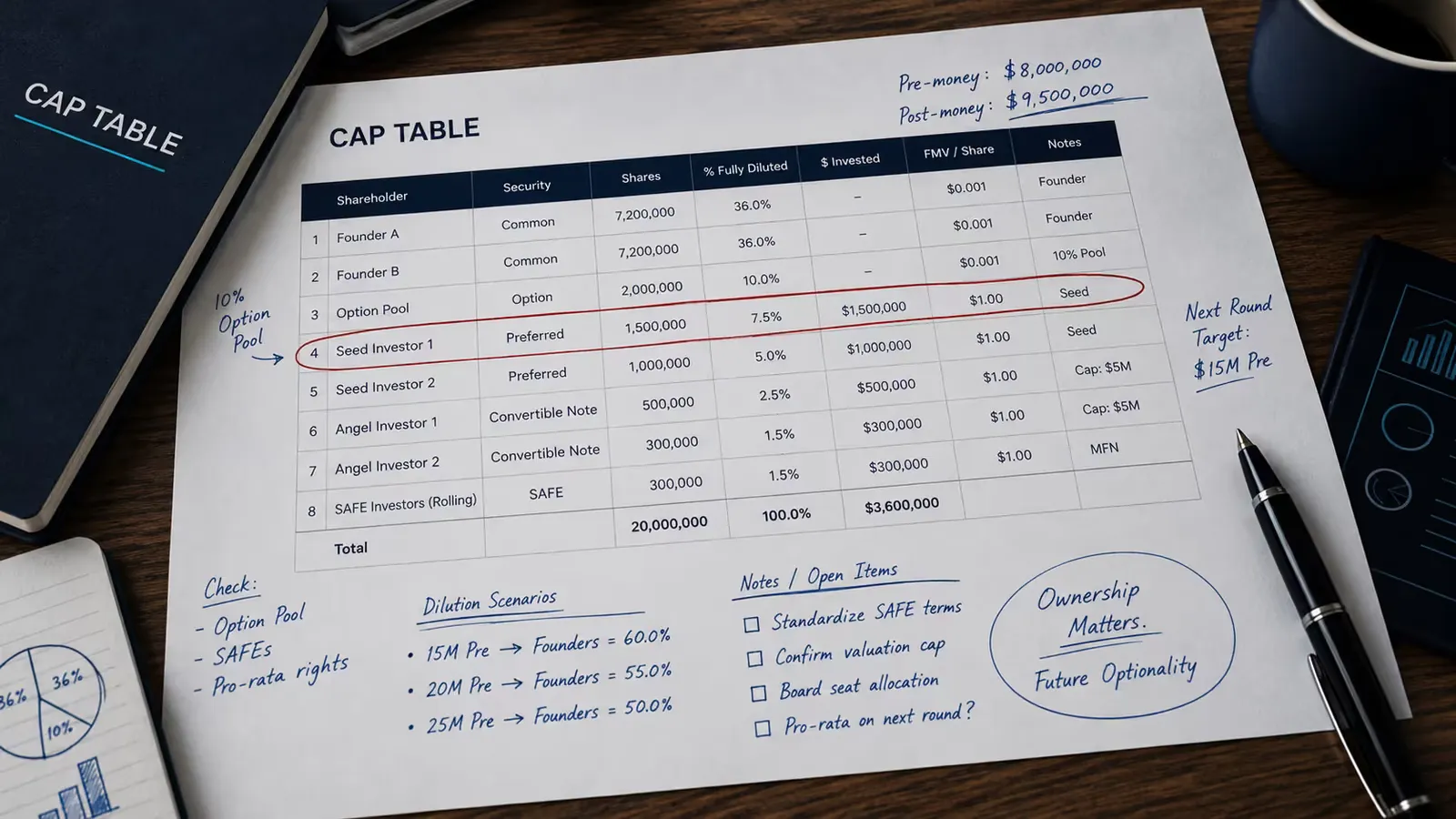

Cap Table Red Flags: The Silent Deal-Killers in MENA Fundraising

The cap-table structures that quietly scare off GCC investors — and how to fix them before you raise.

15 Oct 2025Read Post →

M&A Valuation: How Your Business Is Priced — and How to Defend the Number

Three valuation methods, three different numbers, all defensible. Which one ends up in the term sheet — and how the buyer's analyst quietly picks the lowest.

19 Sept 2025Read Post →

M&A Deal Structure: A Seller's Guide to What You Actually Take Home

Two deals, same headline price — a double-digit gap in what reaches the seller's account. Share vs asset sale, earnouts, escrow, locked-box: deal structure from the seller's chair.

29 Aug 2025Read Post →How to Prepare Your Business for Sale: A Complete Guide

Buyers pay a premium for businesses prepared to be bought — and walk from the rest. Valuation, diligence, and negotiation, in the order they actually matter.

15 Aug 2025Read Post →

Private Equity Value Creation: The Playbook, Read From the Founder's Chair

A PE fund prices your business for what they can do with it. The four value-creation levers read from the founder's side of the table — and which ones to pull yourself, before the deal.

15 Aug 2025Read Post →

M&A Negotiation Tactics Every Business Owner Should Know Before Selling

The buyer across the table negotiates acquisitions monthly. You will do this once. Sell-side M&A negotiation tactics: anchoring, the LOI, and re-trade defence.

18 Jul 2025Read Post →

12 Questions to Ask a Potential Acquirer Before You Sign (2026)

Founders sign LOIs they regret because they didn't ask the right questions. Twelve questions that surface real intent, terms, and red flags before you commit.

18 Jul 2025Read Post →When to Sell Your Business: 6 Clear Signs It's the Right Time (Expert Guide)

Most founders sell too late — the buyer noticed first. Six signs the timing's right, and a framework when it isn't yet.

18 Jul 2025Read Post →

M&A Due Diligence Checklist: What Buyers Will Ask — From the Seller's Side

Every item a buyer's diligence team will pull on your business — and what it costs when one surfaces dirty: price chips, escrow bumps, re-trades, dead deals.

11 Jul 2025Read Post →

The Merger and Acquisition Process: A 7-Phase Guide for Founders Selling Their Company

The merger and acquisition process from the seller's chair — what happens to you at each phase, what the buyer is doing behind the scenes, and where founders lose value.

11 Jul 2025Read Post →

Trusts vs. Private Trust Companies: Which Structure Gives Gulf Families More Control over Generational Wealth?

Most Gulf families set up offshore trusts and lose control of their wealth a generation later. When a Private Trust Company beats a trust — and when it doesn't.

3 Jul 2025Read Post →

Oil and Gas Private Equity Firms: Investment Opportunities in Dubai

Energy-focused PE in Dubai buys services and infrastructure, not exploration risk. What those buyers actually look for — and how owners get approached-ready.

29 May 2025Read Post →

Private Equity Investment in Artificial Intelligence in the UAE: Transforming Capital into Innovation

Most PE-in-AI commentary is either hype cycles or hand-waving. What's actually being funded in the UAE, what's being passed on, and where the multiples really sit.

1 May 2025Read Post →Why Deals Fall Apart Between LOI and Close — and How to De-Risk Yours

The signed LOI feels like the finish line. It is the start of the deal's most dangerous stretch — where transactions die, and how to keep yours alive.

22 Apr 2025Read Post →Selling to a Competitor, a PE Fund, or a Search Fund in the GCC

Three buyers, three different lives after close. A competitor, a PE fund and a search fund, compared from the seller's chair for a GCC founder.

8 Apr 2025Read Post →Full Sale, Partial Sale, or Recapitalization: A Founder's Guide to Liquidity Options

Selling all, selling some, and recapitalising are three different bets on control, cash today, and your second bite. A founder's guide to liquidity options.

25 Mar 2025Read Post →Red Flags When Buying a Business in the UAE

The deck looked clean. Diligence found one customer behind half the profit, a founder the business could not run without, and gratuity nobody had funded.

11 Mar 2025Read Post →Buy-Side M&A in the Gulf: How Acquirers Source and Screen Targets

The best acquisition you make is usually the one nobody else was bidding on. How disciplined Gulf acquirers source and screen targets off-market.

25 Feb 2025Read Post →What an M&A Advisor Actually Does (Day to Day on a Live Mandate)

Most founders think an M&A advisor 'finds a buyer'. Finding the buyer is maybe a fifth of the job. A walk through what actually happens on a live sell-side mandate — and what you are really paying for.

11 Feb 2025Read Post →How Long Does It Take to Sell a Business in the GCC? A Realistic Timeline

Most founders expect a sale in months. A realistic GCC timeline runs longer — here is what each phase takes, and what you control.

28 Jan 2025Read Post →Strategic Buyer vs Financial Buyer: Who Pays More for Your GCC Business?

Two offers for the same company, shaped completely differently — because one buyer is buying your business and the other is buying your cash flow. How strategic and financial buyers price, what each wants, and which is right for a GCC founder.

14 Jan 2025Read Post →Escrow & Holdbacks: Why Buyers Withhold Part of the Price

A slice of your price sits in an account you cannot touch for a year or more. Why buyers withhold it, and how to negotiate the holdback down.

17 Dec 2024Read Post →Reps & Warranties Explained: What a Seller Is Actually Promising

The price is agreed, then the lawyers send pages of statements you must swear are true. That schedule is where a clean sale becomes a lawsuit — or doesn't.

3 Dec 2024Read Post →Working Capital Pegs & Completion Accounts: Why the Final Price Isn't the Headline

You agreed a number, signed the LOI, then a spreadsheet quietly shaved a chunk off it. The working-capital peg and completion accounts, from the seller's seat.

5 Nov 2024Read Post →

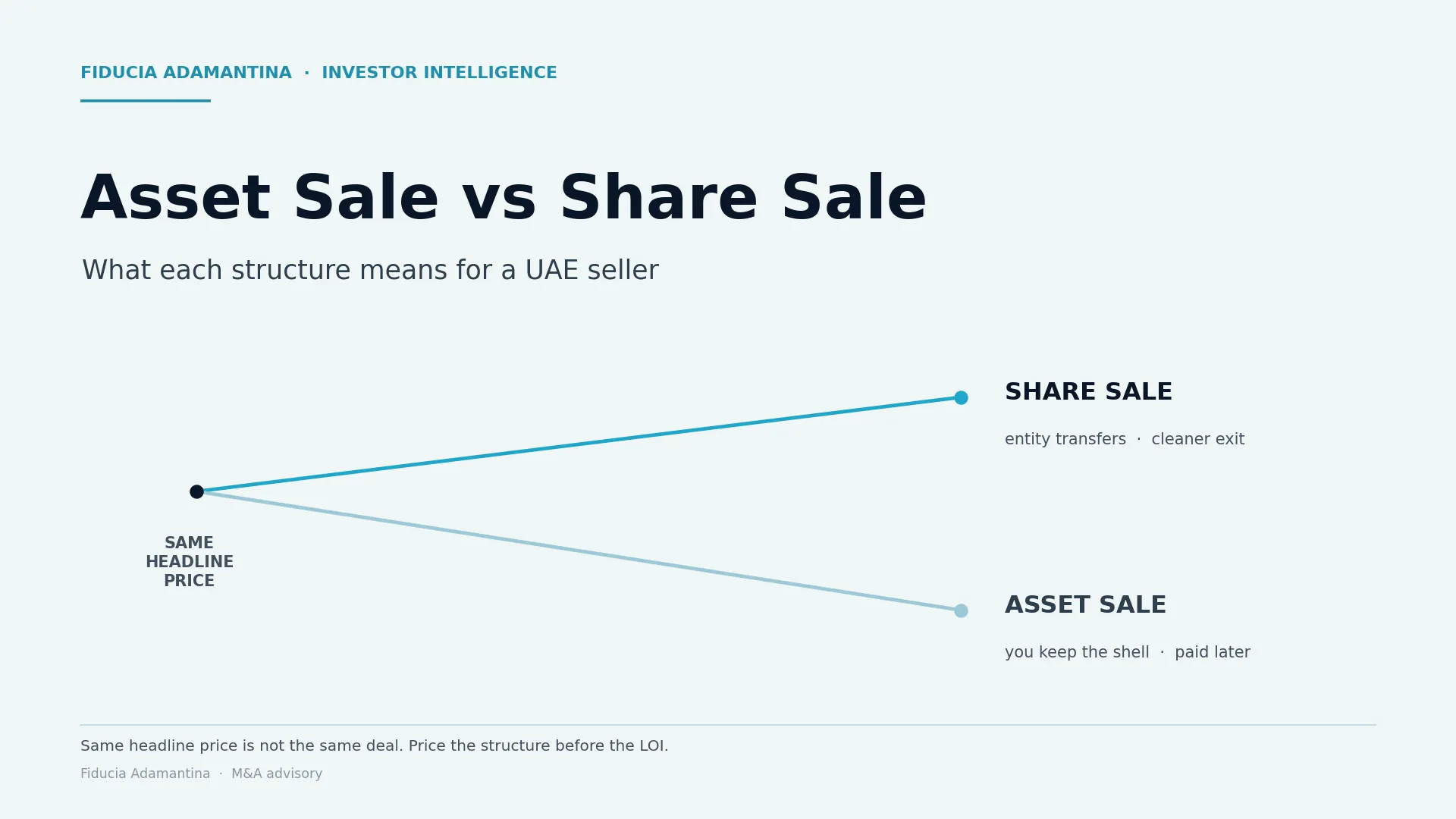

Asset Sale vs Share Sale in the UAE: What Each Means for a Seller

Same price, two deals: one buyer takes your company, one takes its parts. In the UAE that fork decides what you net and how long you spend cleaning up.

8 Oct 2024Read Post →What Is an Earnout — and How They're Structured in GCC Deals

An earnout can bridge a valuation gap — or quietly hand the seller the risk and none of the controls. How they're structured, and capped, in GCC deals.

10 Sept 2024Read Post →The GCC Founder's M&A Glossary: 30 Deal Terms, Plainly Explained

Buyers negotiate in a language built to be one-sided when only one side is fluent. Thirty M&A deal terms — from LOI to escrow to the working-capital peg — explained plainly, from the GCC seller's chair.

13 Aug 2024Read Post →

7 Best Mergers and Acquisitions Companies in Dubai (2026): A Founder's Buyer's Guide

The wrong M&A advisor costs more than fees — it costs the deal. How to test for sector fit, process discipline, and conflicts before you sign.

1 Feb 2024Read Post →

Private Equity Investment in Construction Companies: Emerging Trends in Dubai and Beyond

UAE construction is one of the few sectors where PE money is genuinely chasing operators, not the other way around. What PE wants, and what it pays for.

1 Feb 2024Read Post →Top M&A Advisory & PE Consulting Firms for Founders

Most 'top firms' lists are paid placements. A founder's read on which M&A advisors and PE consultants actually deliver — by sector, deal size, and approach.

1 Feb 2024Read Post →

Private Equity Investment in Fintech: How PE Firms are Transforming Financial Technology

Dubai fintech founders fundraise from the wrong PE firms and waste a year. Who actually backs fintech in the UAE, what they pay, what they ask first.

31 Jan 2024Read Post →Preparing to raise or sell?

Book a confidential strategy call and we’ll point you to the most practical next step.

Book a Strategy Call